Featured

How the WASDE report influenced selling on the soybeans markets

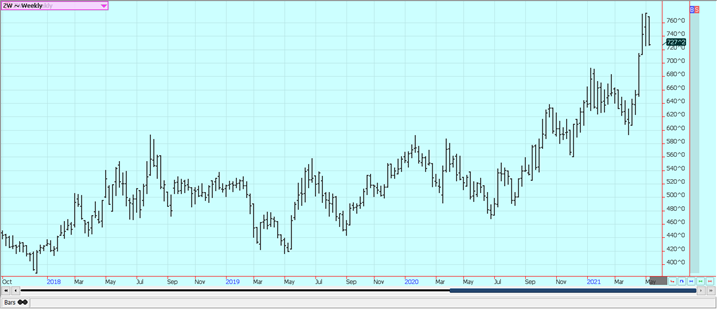

May Soybeans and Soybean Meal closed lower while Soybean Oil was higher. Some of the selling was in response to the WASDE reports released on Wednesday and on news that the Mississippi River was closed at Memphis. The reports showed strong demand for biofuels moving forward. Production was a little less than expected but so was demand. Ending stocks were a little higher than expected but still very tight

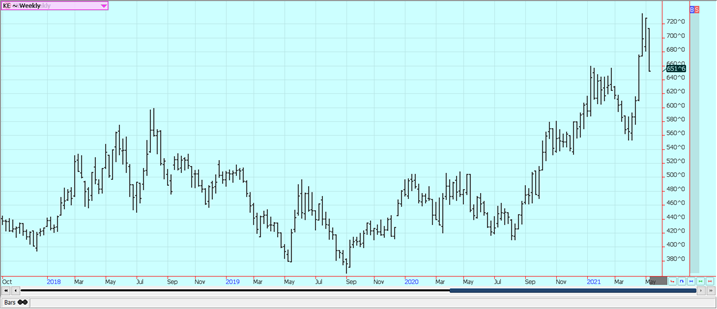

Wheat: Wheat markets were lower and the charts show that a major correction is underway. The reports showed less demand to go with less production. Minneapolis held better as production forecasts are less for Spring Wheat. The dry weather in other parts of the Great Plains did not appear to make much difference to Winter Wheat production and yields. Scattered showers are in the forecast for this week in western Texas. Dry conditions remain in the northern Great Plains and Canadian Prairies. Kansas also got some beneficial precipitation over last weekend and this week. Wheat remains a weather market, but the demand side has been weak. Demand remains disappointing but the production might not be there for better demand in the coming year. Corn prices are high so demand for feed wheat could increase.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

Corn: Corn closed sharply lower last week in response to the USDA WASDE reports released on Wednesday and ideas of weak demand for old crop Corn. The bridge over the Mississippi River was opened for barge traffic to pass through on Friday after being closed on Thursday. A bridge over the river cracked and barges were not able to pass under the bridge. Export sales were poor yesterday for old crop Corn. USDA estimated less demand in its Wednesday reports for the coming year than the trade had expected. USDA expects increased competition from the Black Sea and did not cut Brazil Corn production as much as the trade has figured. The supply-side showed slightly less production than the trade had anticipated but the overall effect was for higher than expected ending stocks estimates. Western sections of the Midwest got crops planted with speed, but eastern areas were slower. Emergence has been about average in all areas. Emergence has been slow due to cold temperatures. Temperatures will be cooler this week and there will be precipitation to keep farmers from the fields. Overall planting conditions should be fairly good over the next week. There are also concerns about the production potential for the Safrinha crop in Brazil as growing areas have been warm and dry and look to stay that way longer term. Reports indicate that crops are being stressed due to the lack of rain. It is drier in central and parts of northern Brazil. The Winter Corn crop progress is well behind normal and it has been dry in major growing areas. There are worries that US Corn is priced out of the world market as US Corn is the highest price of any offering nation, but the lack of production of the second crop in Brazil should mean stronger demand for US Corn. Demand for US Corn has been coming at a stronger pace than estimated by USDA and it looks like US ending stocks can be significantly less than current projections by the end of the year. Demand for ethanol production should increase as people in the US get vaccinated and start to drive again.

Weekly Corn Futures:

Weekly Oats Futures

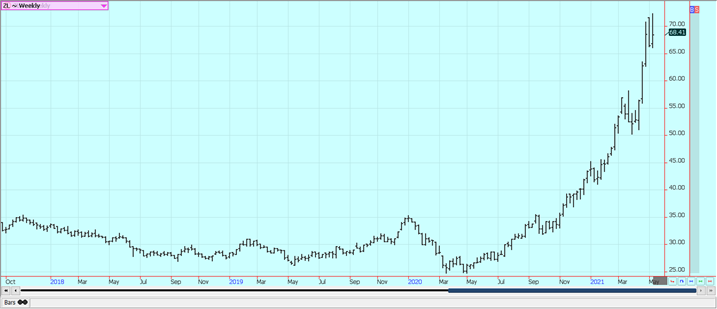

Soybeans and Soybean Meal: May Soybeans and Soybean Meal closed lower while Soybean Oil was higher. Some of the selling was in response to the WASDE reports released on Wednesday and on news that the Mississippi River was closed at Memphis. The reports showed strong demand for biofuels moving forward. Production was a little less than expected but so was demand. Ending stocks were a little higher than expected but still very tight. Estimates for this year were unchanged. A bridge over the river cracked and barges were not able to pass under the bridge. Ideas are that the closing will last only a few days but the market was worried about a longer closure and the possible effects on river shipping. In fact, the government announced that the bridge would be reopened to barge traffic on Friday. Commercials are thought to be the best buyers but did not appear to buy much after the WASDE reports. Funds appeared to be the best sellers on the week. The recent rally has been led by demand amid a very tight stocks situation here in the US. There is still crush demand and a little export demand even though the demand is less now than before. The US does not have a lot of Soybeans in the country anymore as most producers have already sold. Buyers are scrambling for what is left. Brazil is rapidly exporting Soybeans.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

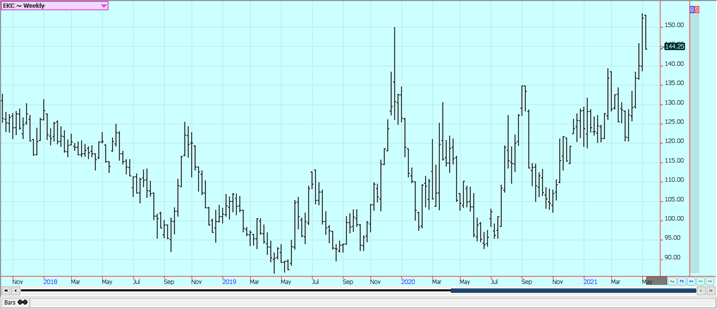

Rice: Rice prices were lower Friday and for the week on what appeared to be follow-through speculative selling due to forecasts for increased precipitation and warmer temperatures for US growing areas. The USDA WASDE reports released on Wednesday were considered neutral to negative for the trade. Rice areas have generally been wet although some parts of Texas could use a little rain. Louisiana is saturated. Temperatures have been cold, especially in Arkansas but the crop has been getting planted and is emerging, anyway. The cash market is working through PL-480 tenders for milled Rice. Texas and Louisiana are almost out of Rice, but there is Rice available in the other states, especially Arkansas. Asian and Mercosur markets were steady to lower last week. New crop months were a little higher but July was the real mover. Mississippi and Arkansas are actively planting around the rains.

Weekly Chicago Rice Futures

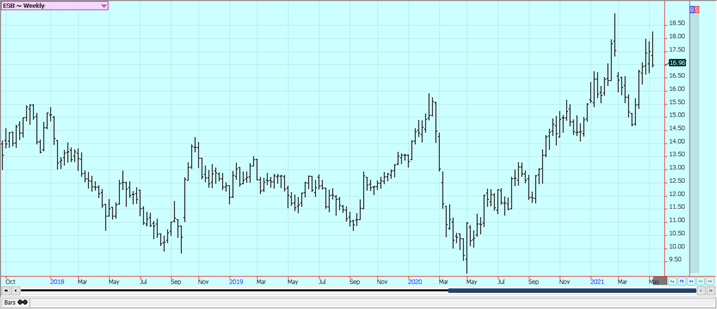

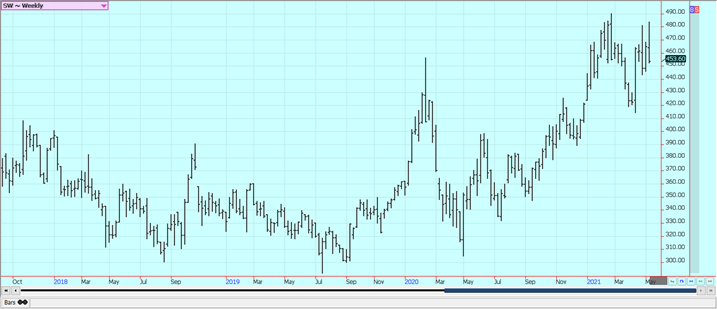

Palm Oil and Vegetable Oils: Palm Oil was closed for Eid the last couple of days last week and traded weaker before that. Supplies in Indonesia are likely to increase this year according to the government there. The private sources showed that export demand is running ahead of last month so far this month, but the market fears the loss of Indian demand due to the big Coronavirus outbreak in India that could cut demand. Ideas of tight supplies are still around but MPOB did show higher than expected ending stocks in its March data. Canola was sharply lower in all months and was weakest in July as demand is feared to be less because of a strong Canadian Dollar but as new crop concerns continued despite improved growing and planting conditions. Worries about South American production are supporting both markets as is dry weather in the Prairies. Some showers were seen in western areas late last week. Demand is thought to be OK with crush margins favoring a lot of production of vegetable oils to feed the demand but less exports. The demand for biofuels is about to increase and is one reason to see much stronger Soybean Oil and Canola prices.

Weekly Malaysian Palm Oil Futures:

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

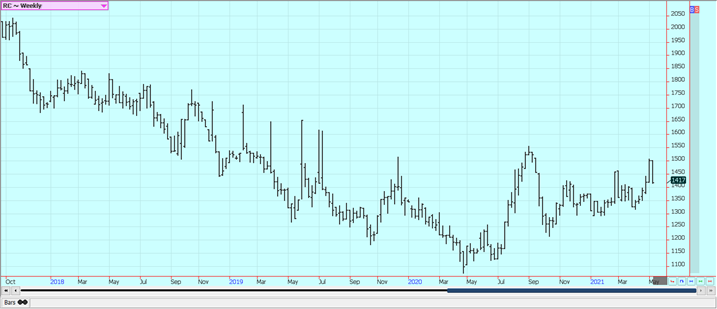

Cotton: Futures were sharply lower once again on shat appeared to be speculative selling tied to weak export sales. Trends have turned down on the daily charts but the weekly charts are holding mixed trends. The WASDE reports released on Wednesday featured a tight ending stocks scenario moving forward for the market. Demand ideas were strong. However, the export sales reports in the last several weeks have been less than hoped for. Support is still coming from dry weather in Texas although the forecasts for the region are improved and resistance from weaker demand as seen in the weekly export sales report. The demand for US Cotton in the export market was weaker once again last week, but has been strong even with the Coronavirus causing disruptions at the retail level around the world. The US stock market has been generally firm to help support ideas of a better economy here and potentially increased demand for Cotton products. It is dry in western and southern Texas. Some showers are reported in western areas to help.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ closed a little higher in range trading on Friday and were higher for the week. Weekly chart trends are turning up. The USDA production reports released on Wednesday made no changes to estimates from last month. The market held support areas on the charts and trends are still trying to turn up on the daily charts. The price action suggests that prices might have gotten too cheap. The weather in Florida is good with a few showers or dry weather to promote good tree health and fruit formation. The hurricane season is coming and a big storm could threaten trees and fruit. That is still a couple of months away. It is dry in Brazil and crop conditions are called good even with drier than normal soils. Stress to trees could return if the dry weather continues as is in the forecast. Mexican crop conditions in central and southern areas are called good with rains, but earlier dry weather might have hurt production. It is dry in northern and western Mexican growing areas.

Weekly FCOJ Futures

Coffee: New York and London were lower on what appeared to be fund selling. The daily charts show downtrends while the weekly charts still show up trends. The current and future Brazil weather remains the focus. Most if not all areas should stay dry for at least the next week. Fears of dry weather impacting Brazil’s production continued to support prices overall. It remains generally dry there and there are still no forecasts for any significant rains in Coffee areas. It was dry at the flowering time as well. It is also the off-year in the two-year production cycle. Production conditions elsewhere in Latin America are mixed with good conditions reported in northern South America and improved conditions reported in Central America. Conditions are reported to be generally good in Asia and Africa. It’s turning a little dry in Southeast Asia including Vietnam.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London were both lower on what appeared to be fund selling and despite drought conditions continuing in Brazil. Both markets could be forming tops on the daily and weekly charts. There is plenty of White Sugar available in India for the market and London has been the weaker market to date. Fears of dry Brazilian weather continued. The primary growing region has been dry in Brazil with little or no rain in the forecast. Production has been hurt due to dry weather earlier in the year. The seasonal crush is off to a slow start and the Sugar content of the cane is reduced in initial industry reports from the center-south of Brazil. India is exporting Sugar and is reported to have a big cane crop this year. Thailand is expecting improved production after drought-induced yield losses last year. The EU had production problems last year but is expecting much better production this year.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

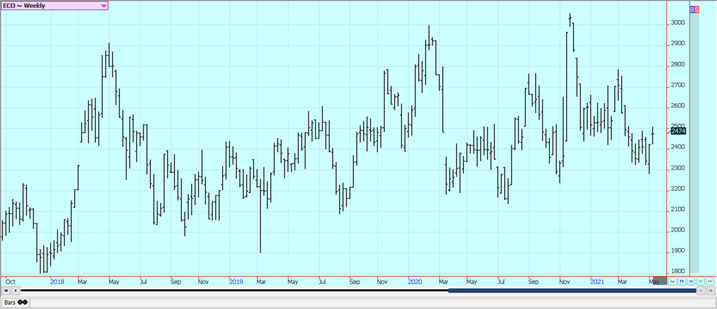

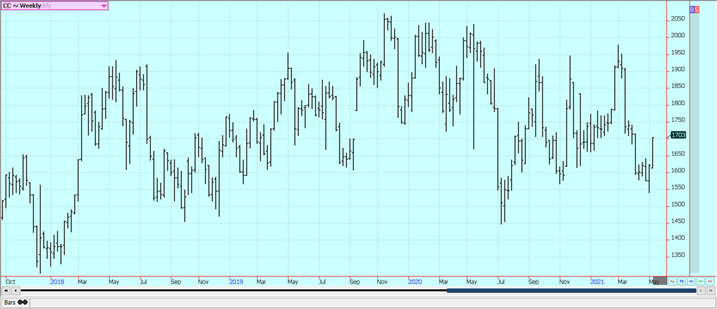

Cocoa: New York and London closed higher last week. Weekly price trends are up in London and are turning up in New York. The harvests are over in West Africa and ports there have been filled with Cocoa. European demand has been slow as the quarterly grind data showed a 3% decrease from a year ago in grindings. This has been caused by less demand created by the pandemic. Asian demand improved. North American data showed improved demand. But, the supplies are there for any increased demand.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

—

(Featured image by 1737576 via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

The TopRanked.io Weekly Digest: What’s Hot in Affiliate Marketing [++ KuCoin Affiliate Program Review]

X now allows people to block certain topics from their feed. This week, we're going to tell you how to...

Hotel Stay Project Supports Wildlife Conservation in Japan

Iwate Prefecture launched a project linking hotel stays to conservation through Morioka Zoological Park Zoomo. A themed room at Yunomori...

Bitcoin Leads Modest Crypto Rebound Amid Mixed Signals

Bitcoin rose 2 percent to above 77000 as ETFs saw 15 million inflows and April gains of 12.2 percent. Ethereum...

Major Pharma Advances: EU Approvals, Vaccine Progress, and Breakthrough Clinical Results

Johnson & Johnson has EU approval for nipocalimab for generalized myasthenia gravis, showing superior control and sustained benefits. Sanofi reported...

Agential Cannabis 2026 to Drive APAC Market Growth and Global Industry Collaboration

Agential Cannabis 2026 will take place September 23–24 in Bangkok, bringing global experts together to advance the APAC medical cannabis...

|

|

|  |

|

|

-

Crypto2 weeks ago

Crypto2 weeks agoBitcoin Holds Steady as Institutions Move In and Crypto Markets Stay Neutral

-

Crowdfunding8 hours ago

Crowdfunding8 hours agoHotel Stay Project Supports Wildlife Conservation in Japan

-

Impact Investing1 week ago

Impact Investing1 week agoClosing the Gap: From Climate Commitments to Urgent Action

-

Biotech3 days ago

Biotech3 days agoOnyx Biotech Secures Pre-Seed Funding to Accelerate AI-Driven Drug Development