Featured

Why the production of most vegetable oils is less this year

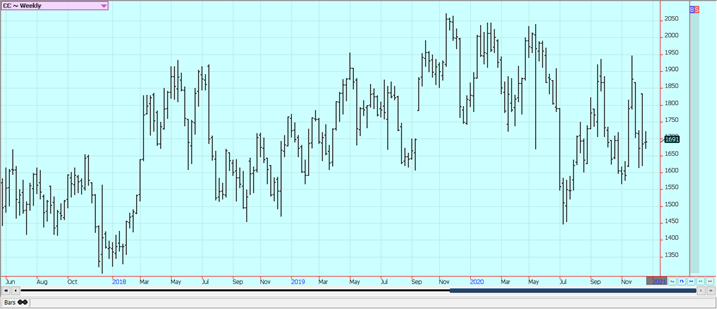

Palm Oil closed higher and made a new high weekly close once again last week. The market was supported by ideas of tight supplies coming down the road. Production of most vegetable oils in the world is less this year due to a lack of production of oilseeds. The production of Palm Oil is down in both Malaysia and Indonesia as plantations in both countries are having trouble getting workers into the fields.

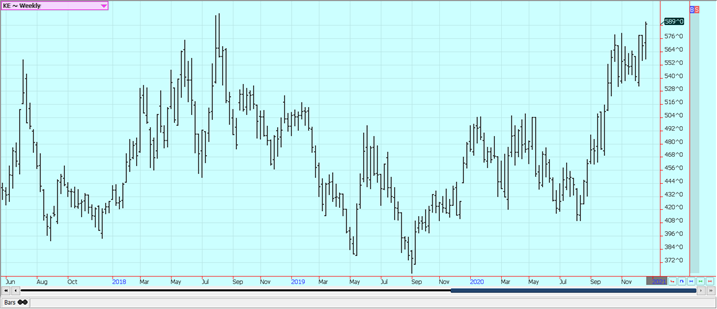

Wheat: Winter Wheat markets were higher last week after a strong rally on Thursday. Minneapolis Spring Wheat contracts closed higher as well, but lagged the strength of the Winter Wheat markets. US prices remain very close to international prices and US markets have searched for new demand. Export demand has started to improve with the close price relationships but remains moderate. World prices have held steady or worked a little higher even with additional supplies available to the market as Russian prices remain elevated. Australian supplies have increased as its harvest is moving forward. US weather is mixed with still dry conditions in the western Great Plains. Some precipitation was reported in the eastern Great Plains and in parts of the Midwest. Parts of southern Russia remain dry.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Chicago Hard Red Winter Wheat Futures

Weekly Minneapolis Hard Red Spring Wheat Futures

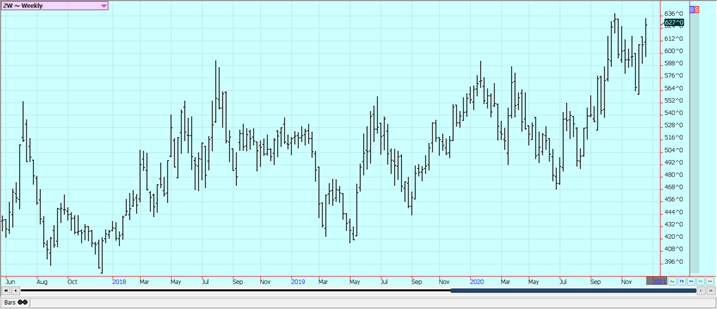

Corn: Corn was higher and trends are still up on the daily and weekly charts. Oats moved sideways. New export demand was weaker and the lowest for the marketing year last week. Export demand has held strong as US Corn is about the cheapest feed grain in the world market. Domestic demand has been less due to reduced demand for ethanol processing and questions about feed demand. It has rained in parts of Argentina and in much of Brazil in the past week. Drought could develop in Brazil and Argentina as the overall weather patterns have been dry and as dry weather is in the forecast for Argentina and southern Brazil. The drought is especially serious in South America for the first Corn crop but the second crop could also be affected due to late planting in central and northern Brazil. Dry weather has delayed the Soybeans planting and that will delay the second Corn planting later.

Weekly Corn Futures:

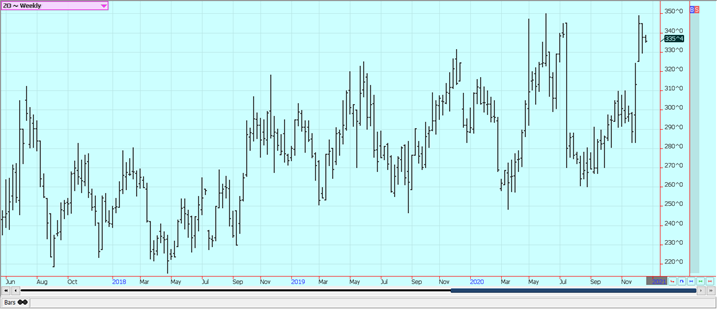

Weekly Oats Futures

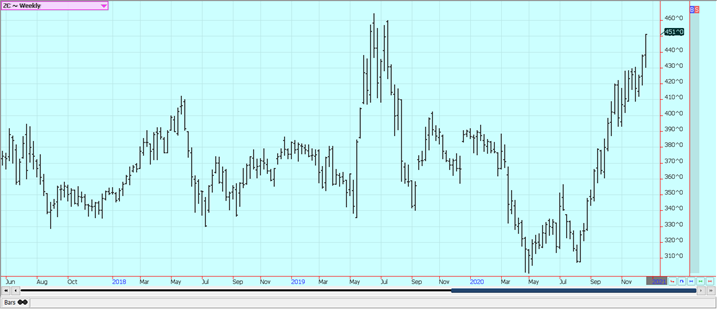

Soybeans and Soybean Meal: Soybeans and Soybean Meal closed higher once again on better demand for US Soybeans and despite rains in South America. The weekly export sales report was in line with expectations but still the lowest amount for the marketing year. US ending stocks estimates are very tight and are likely to get even tighter as time goes on. China continues to buy in small amounts each day but has cancelled and switched some contracts made to unknown destinations. Production potential is being threatened in South America due to the lack of rainfall. The situation is most serious in central and northern Brazil, but has improved in southern Brazil and Argentina due to recent rains. Southern Brazil and Argentina will now turn warm and dry and this will be much more consistent with atypical La Nina pattern. The world will need very strong production from South America to meet the projected demand. The stocks to use ration for Soybeans is now very small and the situation is the tightest projected in years.

Weekly Chicago Soybeans Futures:

Weekly Chicago Soybean Meal Futures

Rice: Rice was lower last week as trading reflected the lack of activity in the domestic cash market. The weekly export sales report featured strong demand overall. Trading volumes have been less for the last couple of weeks. The cash market is slow and the lack of business is reflected in futures volumes traded. Reports indicate that domestic demand has been poor to average with better consumer demand more than offset by much less demand from schools and other institutions.

Weekly Chicago Rice Futures

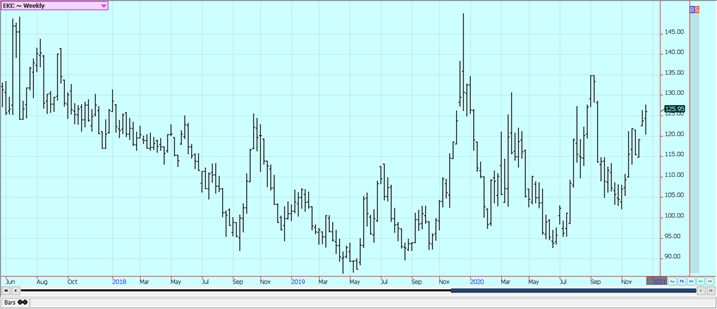

Palm Oil and Vegetable Oils: Palm Oil closed higher and made a new high weekly close once again last week. The market was supported by ideas of tight supplies coming down the road. Production of most vegetable oils in the world is less this year due to a lack of production of oilseeds. The production of Palm Oil is down in both Malaysia and Indonesia as plantations in both countries are having trouble getting workers into the fields. Export demand has been strong and ethanol demand has been moderate. Soybean Oil and Canola were higher on strong demand ideas. Production problems for Soybeans in South America and a strike by workers at ports in Argentina helped Soybean Oil. Very strong Palm Oil prices have made buying Soybean and Canola oils the better option. Trends are up in Soybean Oil and in Canola. Demand for Canola has improved in recent weeks and farm selling has been less.

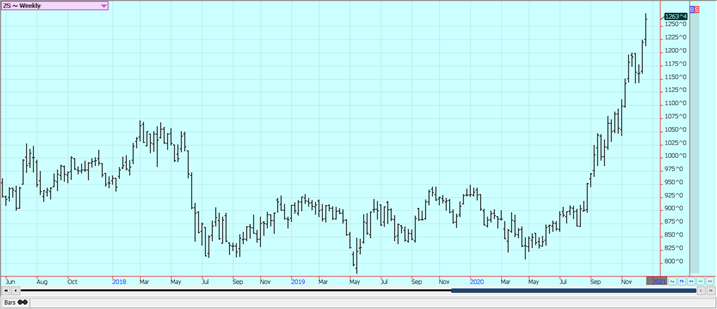

Weekly Malaysian Palm Oil Futures:

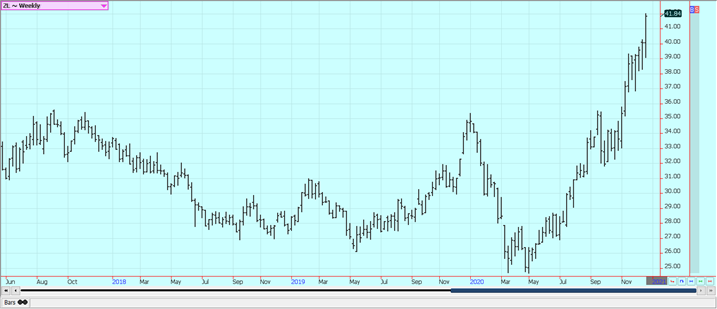

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures:

Cotton: Cotton closed a little lower in consolidation trading last week. Harvest is mostly done amid drier weather conditions in West Texas and the Delta and Southeast. The weekly export sales report showed very strong demand once again last week. Export demand has held strong despite stay at home orders and weaker economies around the world. Traders now hope for even more demand later as the vaccines are given out and the world economies start to recover.

Weekly US Cotton Futures

Frozen Concentrated Orange Juice and Citrus: FCOJ closed a little higher last week. Cold weather is making its way into Florida. The cold is more a reminder of the time of year it is and less an actual threat to trees and fruit. The weather in Florida remains good for the crops. The Coronavirus is still promoting consumption of FCOJ at home. Restaurant and food service demand has been much less as no one is dining out. The weather in Florida is good with frequent showers to promote good tree health and fruit formation. Brazil has been too dry and irrigation is being used. Showers are falling in Brazil now and these need to continue to ensure good tree health. However, it could turn warm and dry again next week. Mexican crop conditions are called good with rains.

Weekly FCOJ Futures

Coffee: Futures were higher last week in both markets. Trends are turning up in both markets. The market is looking ahead to next year. Vietnam has harvested its production under mostly dry conditions. Central America is also drier for harvesting. Brazil is getting some rains now to improve fruit development after an extended dry season, but the rains are sporadic and not everyone is getting helped. The demand from coffee shops and other food service operations is still at very low levels as consumers are still drinking Coffee at home. Reports indicate that consumers at home are consuming blends with more Robusta and less Arabica. The weather is good in Colombia and Peru.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

Sugar: New York and London closed higher and are now probing the upper end of the recent trading range on the charts. It has been raining in south central Brazil and the production of cane is winding down for the season. The first half of December crush was down as cane production has been hurt due to dry weather earlier in the year. Brazil mills have been producing more Sugar and less Ethanol due to weak world and domestic petroleum prices. India has a very big crop of Sugarcane this year. The Indian government has not announced the subsidy for exporters of Sugar so no exports are coming out of India yet. Sources told wire services that any subsidy will need to be significant to get export sales on the books. Thailand might have less this year due to reduced planted area and erratic rains during the monsoon season. The EU is having problems with its Sugarbeets crop due to weather and disease. Coronavirus has returned to the world and has caused some demand concerns, especially for Ethanol.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa: New York closed higher after rebounding from very low levels and London closed slightly higher last week. Importers are still looking for ways to source Cocoa without paying a premium demanded by Ivory Coast and Ghana. Both countries have instituted a living wage for producers there and are looking to tax exports to pay the increased wages. Buyers have been accused of using certified stocks from the exchange instead of buying from origin. There are a lot of demand worries as the Coronavirus is making a comeback in the US. Europe is also seeing a return of the pandemic. However, the grind has held amid good demand from chocolate manufacturers.

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by Quangpraha via Pixabay)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

Abivax Shares Surge as New Trial Data Eases Safety Concerns Over Ulcerative Colitis Drug

Abivax shares surged nearly 36% after positive updated trial results for its ulcerative colitis drug obefazimod reassured investors following earlier...

El Dorado Raises $9M to Expand Cross-Border Fintech Platform

El Dorado, a Latin American fintech improving cross-border financial services, raised a $9 million Series A led by Paradigm with...

Bitcoin Stalls Near $60K as Strategy Moves, ETFs Outflow, and EU MiCA Rules Take Effect

Bitcoin hovers near $60,000 with ETF outflows, while Strategy boosts reserves, sells BTC, and raises dividends to reassure investors. Ethereum...

Cannabis Dominates Global Drug Use: Trends, Risks, and Shifting Markets

Cannabis remains the world’s most widely used illicit drug, with 256 million users in 2024, surpassing all others combined. Growth...

Italy Approves First Hydrogen-Powered Train for National Rail Network

ANSFISA has approved Italy’s first hydrogen-powered train, the Alstom HMU214, for use on the Brescia–Iseo–Edolo line. Capable of 140 km/h,...

|

|

|  |

|

|

-

Impact Investing1 week ago

Impact Investing1 week agoEdison Accelerates Renewable Growth and ESG Impact in 2025

-

Cannabis7 days ago

Cannabis7 days agoSpain Cannabis Laws: Private Use, Fines, and Grey Areas

-

Crowdfunding2 weeks ago

Crowdfunding2 weeks agoWyrmgold Launches Crowdfunding Campaign for Believe in me! (please)

-

Business2 days ago

Business2 days agoDow Jones Near Highs Signals Strength Until Volatility Returns