Markets

Global Sugar Market Strengthens on Supply Growth and Surplus Outlook

Sugar prices rose in New York and London last week. Global supply outlook is strong due to favorable cane and beet conditions and strong Brazil output, despite rain in the north. A large 2025/26 surplus is expected with higher production in India and Thailand. India may export 1.5 million tons, while China keeps imports at 5 million tons.

Wheat: Wheat closed lower yesterday in response to the USDA WASDE and production reports. The market expected to see increased ending stocks estimates but the increase in ending stocks on the US and world data were much larger than anticipated. US ending stocks were estimated at 901 million bushels and world stocks were estimated at 271.4 million tons.

There has been no new China demand news or rumors and the weekly export inspections were down. The weekly USDA reports have started again but USDA is currently releasing old data and not current sales. Southern hemisphere crops appear to be good.

Weekly Chicago Soft Red Winter Wheat Futures

Weekly Kansas City Hard Red Winter Wheat Futures

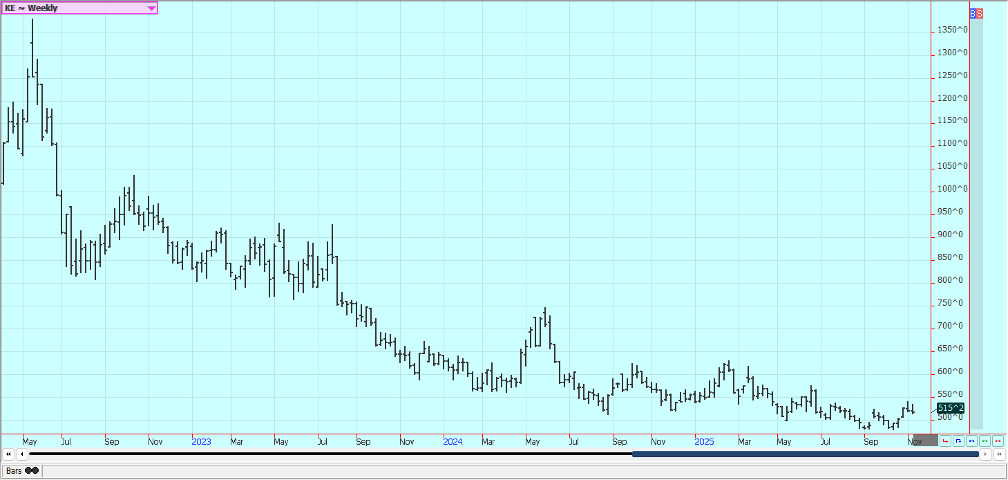

Weekly Minneapolis Hard Red Spring Wheat Futures

Unavaiable today

Corn: Corn was higher last week on ideas and reports of strong export demand. However, prices fell on Friday and gave back most of the gains of the week in response to the WASDE reports. USDA showed higher than expected production at 16.752 billion bushels and higher than expected ending stocks at 2.154 billion bushels. Export demand was increased by 100 million bushels but domestic demand was left unchanged Trends are now mixed in the market.

The weekly export sales report from late September showed that Corn demand held strong. USDA will issue additional reports this week. The harvest is winding down in all areas of the Midwest. There are ideas that US production might not be super strong due to disease such as rust to offset the demand losses. Temperatures should average near to above normal this week and there are forecasts for some rain early this week. Oats were higher last week.

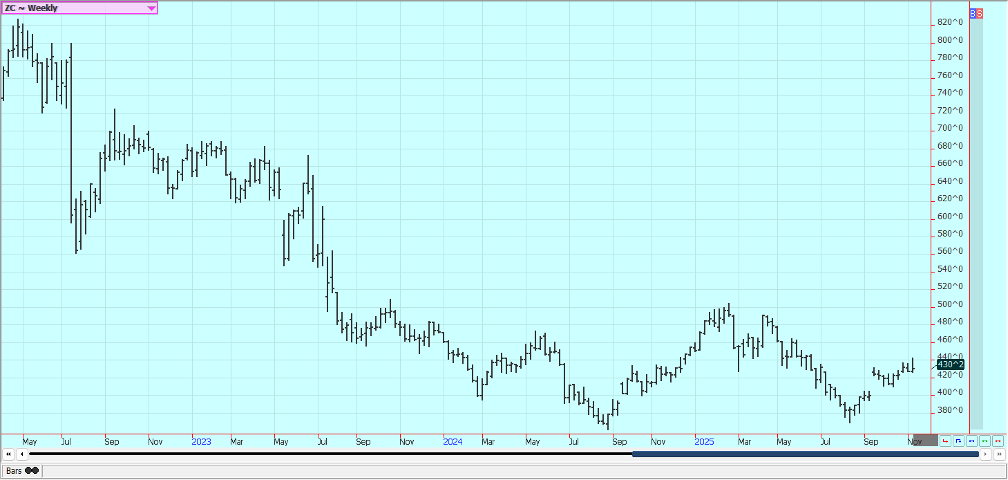

Weekly Corn Futures

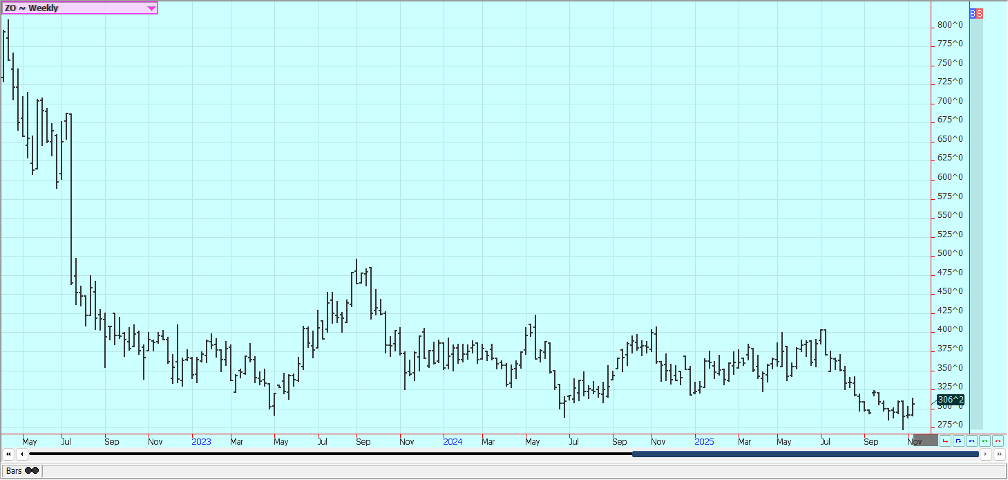

Weekly Oats Futures

Soybeans and Soybean Meal: Soybeans and the products were higher last week on hopes for new Chinese demand, but lower on Friday in response to the USDA reports. USDA estimated production below trade expectations at 4.253 billion bushels and ending stocks just below trade expectations at 290 million bushels. Domestic demand was unchanged but USDA cut export demand and apparently does not think China will be a big buyer of US Soybeans in the near term. There was no talk of new Chinese demand although the market hopes for more.

China bought cargoes over a week ago but has not been reported to buy anything since. China is almost done with purchases for this year and as the US will have to compete with South America for sales in a diminishing Chinese market. The Chinese hog herd is being reduced and this means less demand for Soybeans and Soybean Meal.

The US government has announced that it will support farmers with money, but so far no money has been flowing. Forecasts call for precipitation to be seen in the Midwest. Temperatures will average near to above normal this week. Export demand remains less for US Soybeans as China has been taking almost all the export from South America due to the Trump tariff regime.

Weekly Chicago Soybeans Futures

Weekly Chicago Soybean Meal Futures

Rice: Rice was higher on Friday and higher last week. USDA noted reduced production for All Rice at 207.3 million cwt and for Long Grain at 152.7 million cwt. Demand was unchanged and ending stocks were down to 51.9 million cwt for All Rice and 36.0 million cwt for Long Grain. Iraq has bought 88,000 tons of milled Rice last week. Ideas are that the market is too cheap and that farmers have sold what needs to be sold for now.

The recent selling has been to be relentless and appears tied to the weaker prices in Asia and especially India. Trends are down in the market. The harvest is wrapping up in the delta and Mid South. California is also about done with its harvest. Yields and quality are mixed, but quality appears better than a year ago. The cash market has been slow with low bids from buyers in domestic markets and average or less export demand.

Weekly Chicago Rice Futures

Palm Oil and Vegetable Oils: Palm Oil futures were a little higher last week. Futures reacted to the stronger Ringgit and weaker Chicago prices late in the week and MPOB data from early in the week that showed less than expected ending stocks for the month. There was some buying seen on Indonesian plans to increase the use of Pam Oil in biofuels blends.

There are ideas of increasing supplies, but those ideas are now turning as production enters a seasonal slowdown. There are still ideas of increasing production. The market sentiment overall is turning bearish on ideas of increasing stocks to the market and on some concerns about demand Canola was a little higher. Trends are mixed on the daily charts and are turning up on the weekly charts.

Weekly Malaysian Palm Oil Futures:

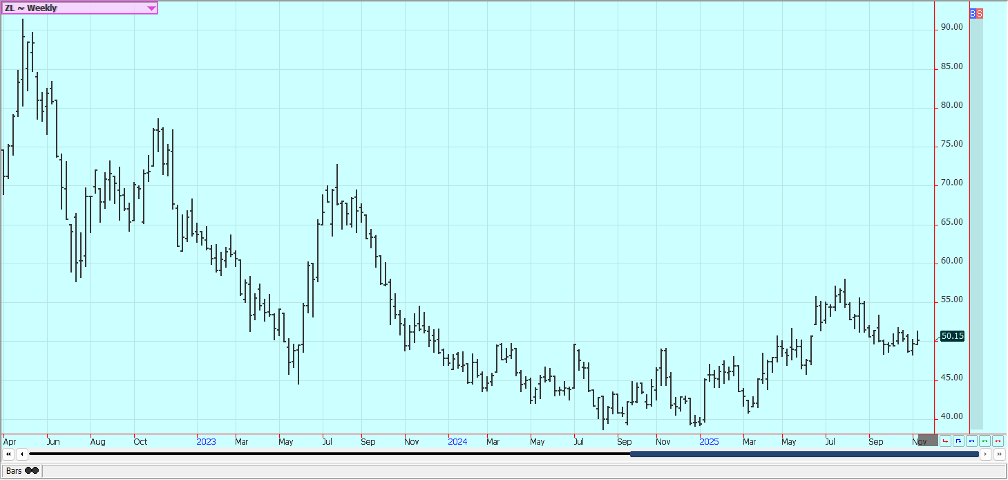

Weekly Chicago Soybean Oil Futures

Weekly Canola Futures

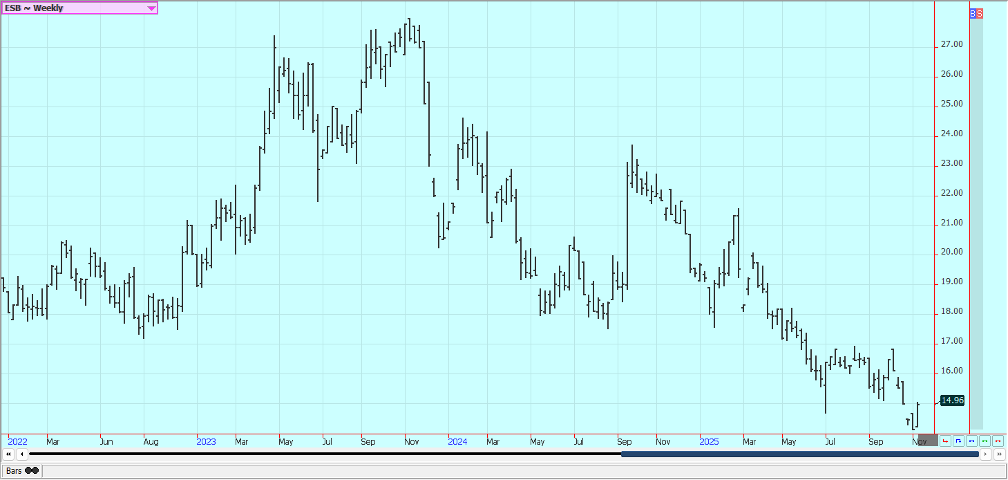

Cotton: Cotton was lower last week in response to the USDA reports that showed higher than expected production at 14.23 million bales. Demand was increased by 20 million bales, but ending stocks were sharply higher at 4.4 million bales.. A lack of new Chinese demand since the event ofthe lower tariffs created some selling interest. US tariffs are now being decided by the Supreme Court.

An end to the tariff wars could start demand for US Cotton in world markets again. The US government is now open again and USDA reports will be released over the next few weeks. The US harvest is over in most areas and initial yield reports are positive. The monsoon in India is good and a good production there is possible.

Weekly US Cotton Futures

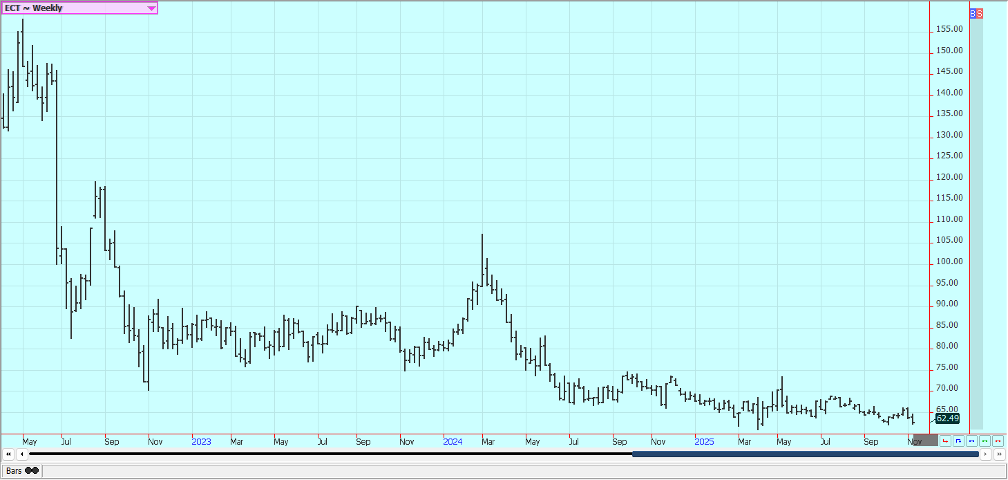

Frozen Concentrated Orange Juice and Citrus: Futures were lower last week and the trends are starting to turn down on the daily and weekly charts. The US government is open again after Congress passed funding bills and the president signed the bills. Secretary Bessent said that certain products will get reduced tariffs soon to help lower prices.

FCOJ from Brazil has been subjected to a 50% tariff that was reduced and could be reduced further by the changes announced. The weather is considered good for production here and in Brazil and Mexico. Development conditions are good in Florida and in Brazil now with occasional showers in Florida and dry weather in Brazil.

Weekly FCOJ Futures

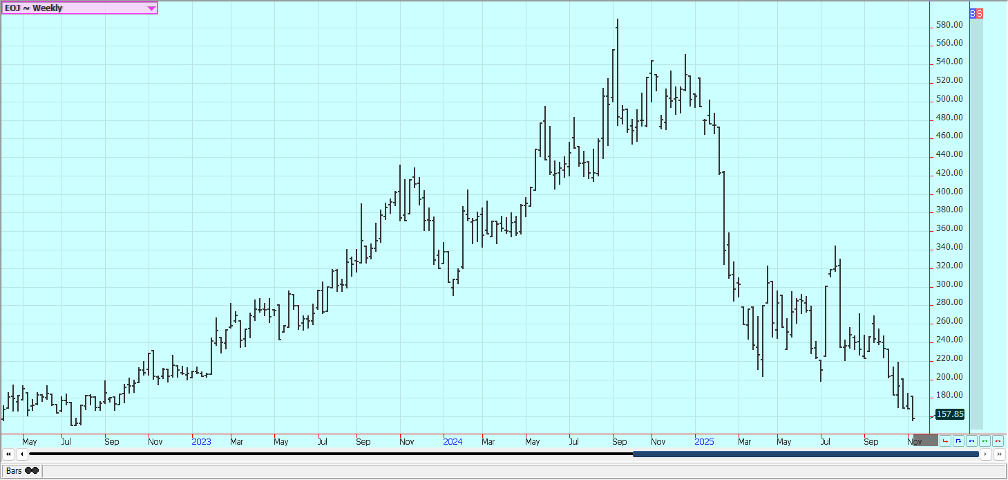

Coffee: New York and London were lower last week on selling due to tariff concerns. Secretary Bessent said that certain products will get reduced tariffs soon to help lower prices. Coffee from Brazil has been subjected to a 50% tariff that could be reduced a lot by the changes announced. It has been a little too dry in Brazil for best yield potential. Vietnam has seen too much rain as typhoons hit the country, but rain is returning to more normal levels now.

Activity remained quiet in Vietnam on limited supplies as offers of fresh beans from the current harvest have yet to pick up. Vietnam exported 1.31 million metric tons of coffee over the January-October period, up 13.4% from a year earlier. A revision of the 50% U.S. tariff on Brazilian imports, including coffee, could push arabica prices lower. Exports of coffee from Brazil totaled 4.14 million 60-kg bags in October, down 20% from last year. Year to date exports are now 33.28 million bags, from 41.77 million last year.

Weekly New York Arabica Coffee Futures

Weekly London Robusta Coffee Futures

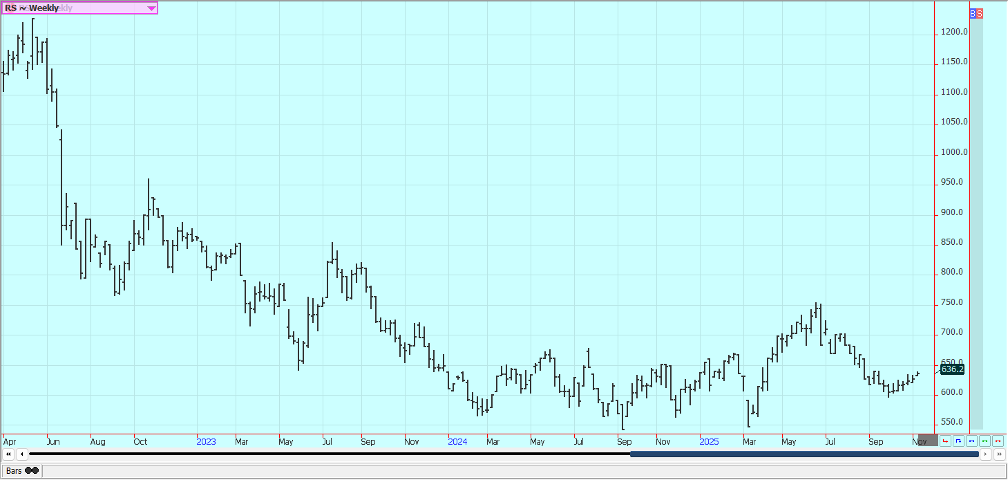

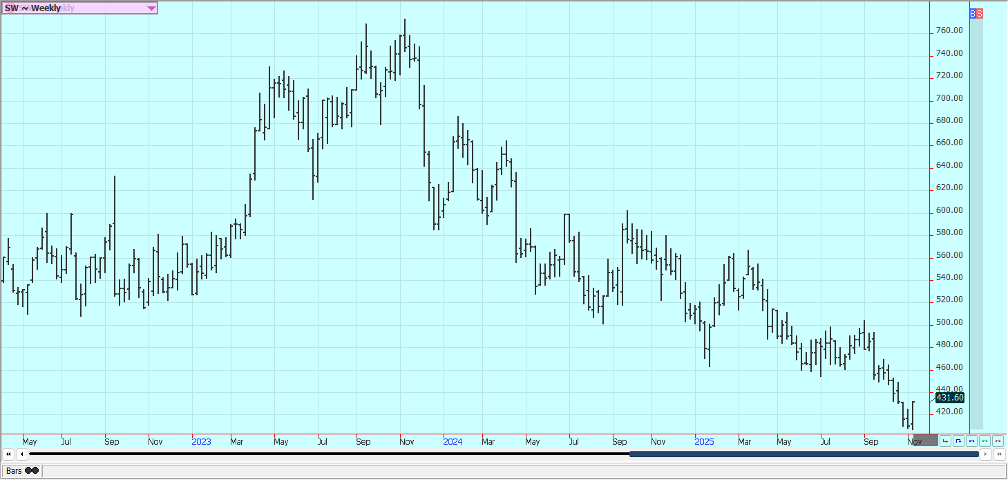

Sugar: New York and London were higher last week. Ideas of good sugar supplies for the market from good growing conditions for cane and beets around the world continue. Sugar production in Center-South Brazil has also been strong, but the south center harvest is almost over. Too much rain has been reported in northern areas.

The prospect of a big global sugar surplus in the 2025/26 season was keeping the market on the defensive with a rise in production in India and Thailand set to increased sugar supplies while global consumption is expected to remain steady.

India plans to allow sugar exports of 1.5 million metric tons in the new season as a decline in the diversion of sugar for ethanol production is expected to leave a larger domestic surplus. China kept its 2025/26 sugar imports forecast unchanged at 5 million tons.

Weekly New York World Raw Sugar Futures

Weekly London White Sugar Futures

Cocoa: New York and London closed lower last week and trends are turning down in both markets. A big main crop harvest is anticipated in West Africa. Demand concerns in West Africa continue. Light rains mixed with heat in Ivory Coast’s cocoa-growing regions last week signaled a positive outlook for the main crop. There are still reports of increased production potential in other countries outside of West Africa, including Asia and Central America.

The market feels that there is less demand and the lack of demand is expected to continue. Malaysia and the US have apparently agreed to allow Malaysi-an Cocoa into the US with 0 tariffs. Cocoa arrivals in ports in top grower Ivory Coast were picking up after a slow start to the season. A total of about 107,000 tons were delivered between November 3 and November 9, up from 90,000 tons in the same week of the previous season,

Weekly New York Cocoa Futures

Weekly London Cocoa Futures

__

(Featured image by Daniel Kraus via Unsplash)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions, including with regards to potential earnings in the Empire Flippers affiliate program. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures.

Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever.

Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

The TopRanked.io Weekly Digest: What’s Hot in Affiliate Marketing [++ KuCoin Affiliate Program Review]

X now allows people to block certain topics from their feed. This week, we're going to tell you how to...

Hotel Stay Project Supports Wildlife Conservation in Japan

Iwate Prefecture launched a project linking hotel stays to conservation through Morioka Zoological Park Zoomo. A themed room at Yunomori...

Bitcoin Leads Modest Crypto Rebound Amid Mixed Signals

Bitcoin rose 2 percent to above 77000 as ETFs saw 15 million inflows and April gains of 12.2 percent. Ethereum...

Major Pharma Advances: EU Approvals, Vaccine Progress, and Breakthrough Clinical Results

Johnson & Johnson has EU approval for nipocalimab for generalized myasthenia gravis, showing superior control and sustained benefits. Sanofi reported...

Agential Cannabis 2026 to Drive APAC Market Growth and Global Industry Collaboration

Agential Cannabis 2026 will take place September 23–24 in Bangkok, bringing global experts together to advance the APAC medical cannabis...

|

|

|  |

|

|

-

Business1 week ago

Business1 week agoThe TopRanked.io Weekly Digest: What’s Hot in Affiliate Marketing [uMobix Affiliates Review 2026]

-

Biotech2 weeks ago

Biotech2 weeks agoBeeline Medicines Launches with $300M to Advance Precision Therapies for Autoimmune Diseases

-

Crypto2 days ago

Crypto2 days agoCrypto Markets Steady as US Bitcoin Reserve Plans and MegaETH Debut Take Focus

-

Fintech1 week ago

Fintech1 week agoFintech Investment Rebounds in 2025 Amid Cautious Optimism for 2026