Business

Texas and Louisiana report excellent rice yields; Cotton down due to choppy trading

World’s stock of rice increased to 144.4 million tons while despite low cotton prices, harvest has been active in the south.

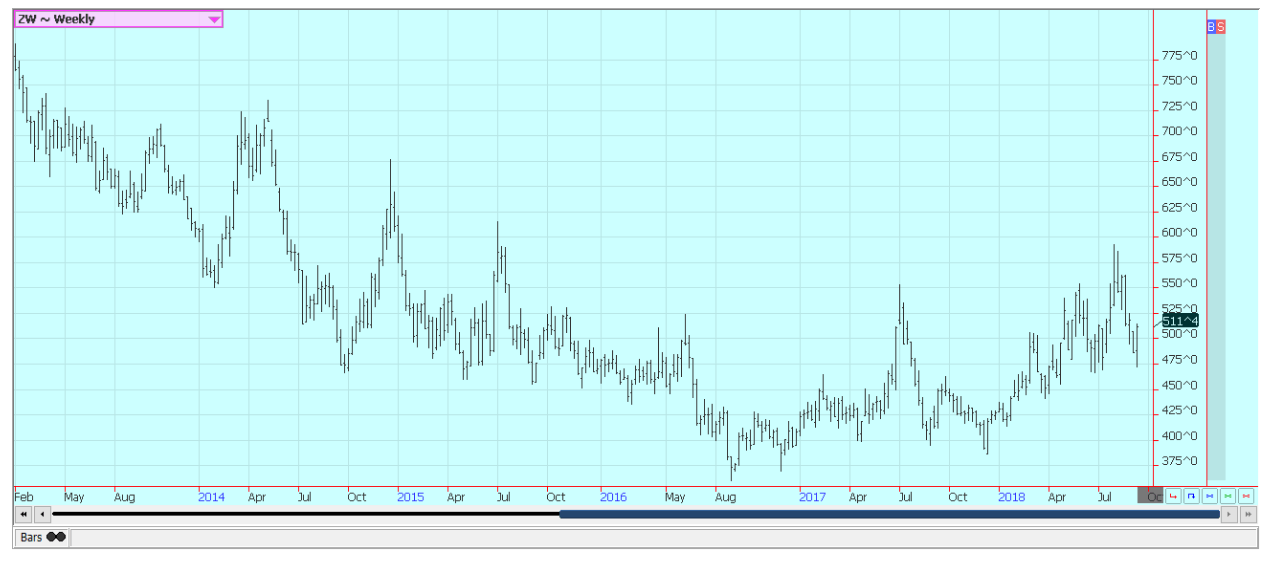

Wheat

Wheat markets were higher on indications that the Russian government might finally be making moves to make exports more difficult. The government announced it is checking exports more thoroughly to ensure that the proper quality is being exported.

The charts still show down trends on the daily charts, but the weekly charts show reversal formations due to the change in months and the expiration of September futures. The market keeps it focus primarily on Russia and the prices it sells wheat into the world market, and especially to Egypt. In fact, Russian wheat exports have been very strong so far this year. Meanwhile, US export sales continue at an average pace and will need to increase to create some speculative buying enthusiasm.

USDA released updated supply and demand estimates on Wednesday. US domestic supply and demand estimates were unchanged and as expected. USDA surprised the trade by showing very strong world production estimates at a time when almost all exporters have sharply reduced production ideas.

For example, European Union production was unchanged at 137.50 million tons against EU estimates closer to 131 million tons. Canadian production was cut by 1.0 million tons, and Australian production was cut 2 million tons, but the market had expected bigger cuts. Russian and FSU-12 production were increased by 3.0 million tons and 3.5 million tons, respectively, at a time when the trade was looking for lower production.

USDA claims that the spring wheat production in Russia and the FSU-12 is much better than expected. This made ending stocks projections above 261 million tons from almost 259 million tons last month and trade expectations of about 257 million tons. USDA did not release new production estimates as it will wait for the small grains report at the end of the month to offer updates.

The weather in the U.S. is improved for planting the next winter wheat crop as much of the Great Plains has seen rains in the last couple of weeks. The U.S. and Canadian spring wheat harvests are moving forward, and the trade expects a smaller crop this year due to stressful growing conditions during the summer.

Weekly Chicago Soft Red Winter Wheat Futures © Jack Scoville

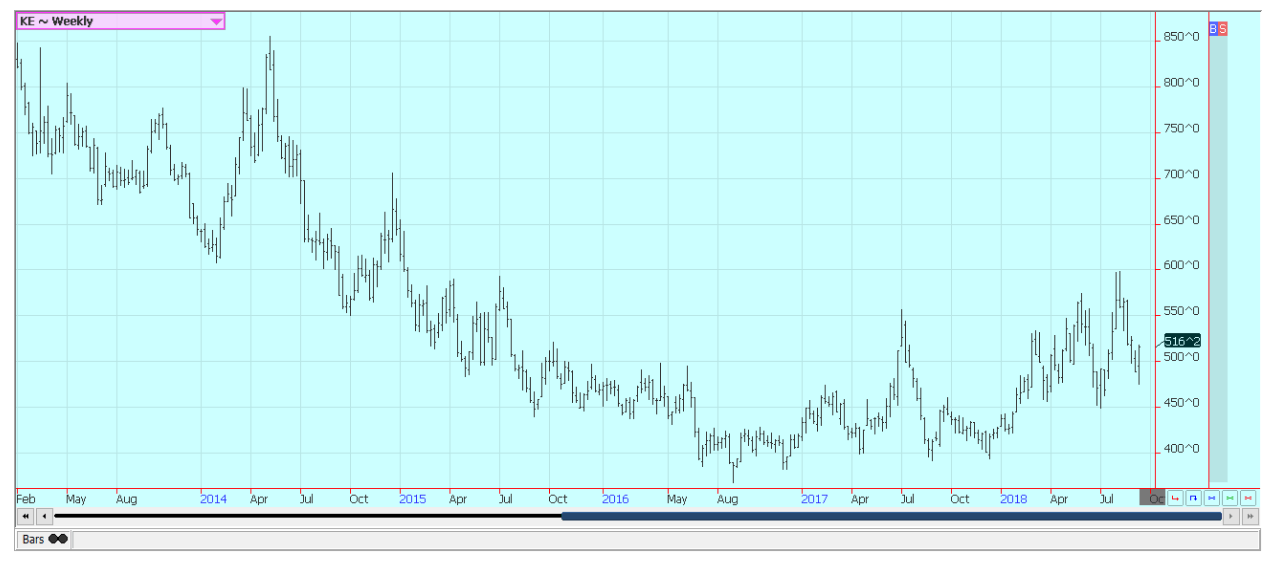

Weekly Chicago Hard Red Winter Wheat Futures © Jack Scoville

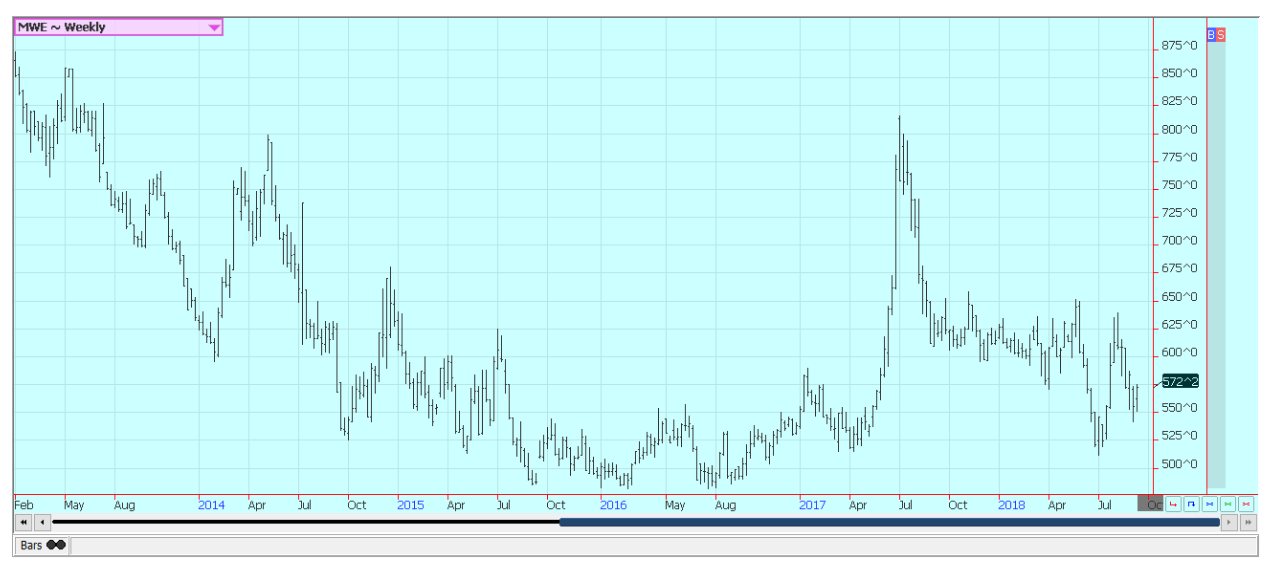

Weekly Minneapolis Hard Red Spring Wheat Futures © Jack Scoville

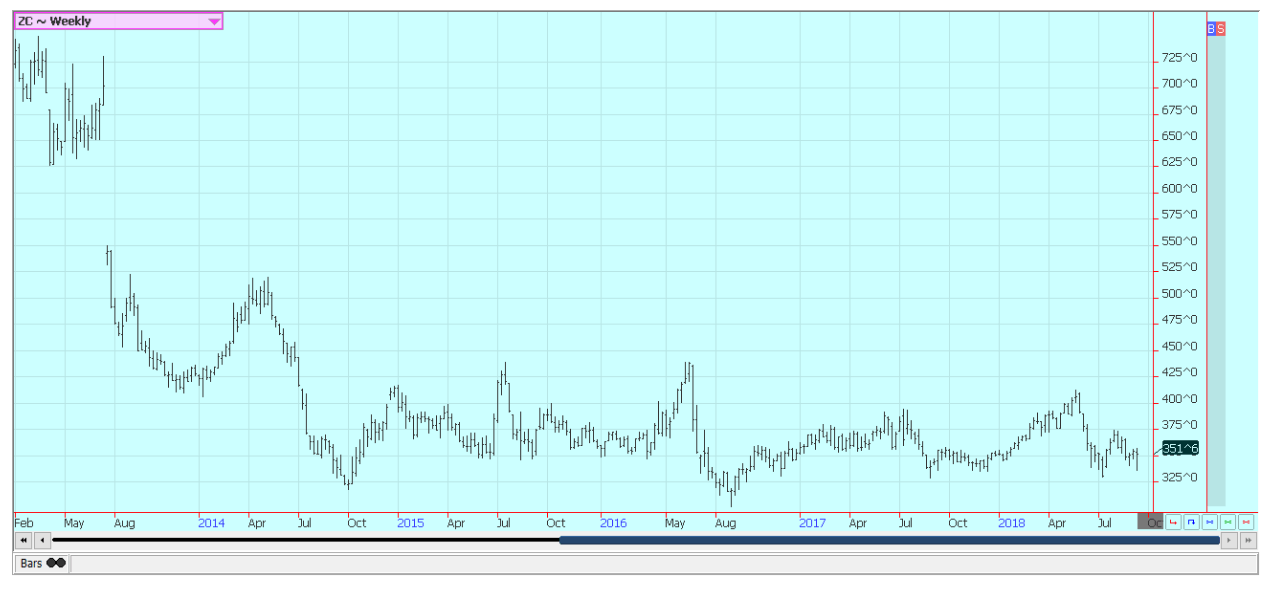

Corn

Corn was a little lower for the week and in response to the USDA reports. USDA surprised the market on Wednesday when it increased production and ending stocks estimates. The USA increased yields to over 181 bushels per acre instead of a slight reduction as expected by the trade. That pushed production to 14.827 billion bushels, well above the highest trade guess.

USDA increased demand for U.S. corn in all domestic and export categories, so ending stocks were increased to 1.774 billion bushels, a significant increase but less than implied by the big production. World ending stocks levels were also increased, mostly due to the bigger projections in the U.S.

The trade is already questioning some of the yield projections made by USDA as the state comparisons show a sharp increase in productivity in the eastern corn belt and increased productivity in the west. The trade will monitor reports from the field and will adjust their ideas according to that data and how it relates to the USDA projections.

The Midwest could feature variable but somewhat disappointing yields once the harvest gets active there in the next few weeks. Rainfall patterns have been very tropical this year, and have featured excessive rains in some areas and dry weather in others. It has been a warm summer as average temperatures have generally been a few degrees above long-term averages.

The warm temperatures have kept plants active and have pushed maturity forward by up to two weeks or so. This usually means less yield at harvest and is the opposite of last year when cool weather allowed the corn to mature slowly and add test weight and yield to the plants. U.S. corn export sales remain very strong and were over 1.0 million tons again last week. Mexico has remained in the market and remains the largest buyer of U.S. corn in the world market.

Weekly Corn Futures © Jack Scoville

Weekly Oats Futures © Jack Scoville

Soybeans and soybean meal

Soybeans were near unchanged last week while soybean meal was lower. USDA estimated soybeans production and ending stocks levels in the U.S. within trade expectations at 4.693 billion bushels and 845 million bushels. There is a big crop coming, but perhaps not as big as feared by the trade, and a relief rally was seen on Wednesday after the report was released.

USDA increased domestic and export demand for the year that is just concluding and increased domestic demand for the new crop year. Even so, 845 million bushels means that there will be a lot of soybeans in the U.S. and that means upside movement in prices should be limited. The Trump administration on Wednesday reached out to China and offered to start talks again, this time in China. That news created some buying interest.

President Trump had previously announced that new tariffs are coming in the very near future and that the new tariffs could total about $200 million. He said he is prepared to bring another round of punitive tariffs against the Chinese that would cover another $267 billion in the near future.

The Chinese show no signs of giving in, and compromise from the U.S. point of view seems unacceptable. The big loser in all of this is the U.S. farmer, who is getting far less for his soybeans than any other producer in the world. USDA has announced supports, but the supports will cover only a part of the losses.

And, China will most likely look for as many other sources for soybeans in the short term and long term as possible, even though they will still need to buy some soybeans here. They will buy as little as possible here while the ramp up efforts in places like Africa to develop agriculture to feed their people. The U.S. farmer is the big loser in the Trump trade wars, and could be a loser in the battles for both the short and the long-term as supplies should be very high and prices will remain very low.

Weekly Chicago Soybeans Futures © Jack Scoville

Weekly Chicago Soybean Meal Futures © Jack Scoville

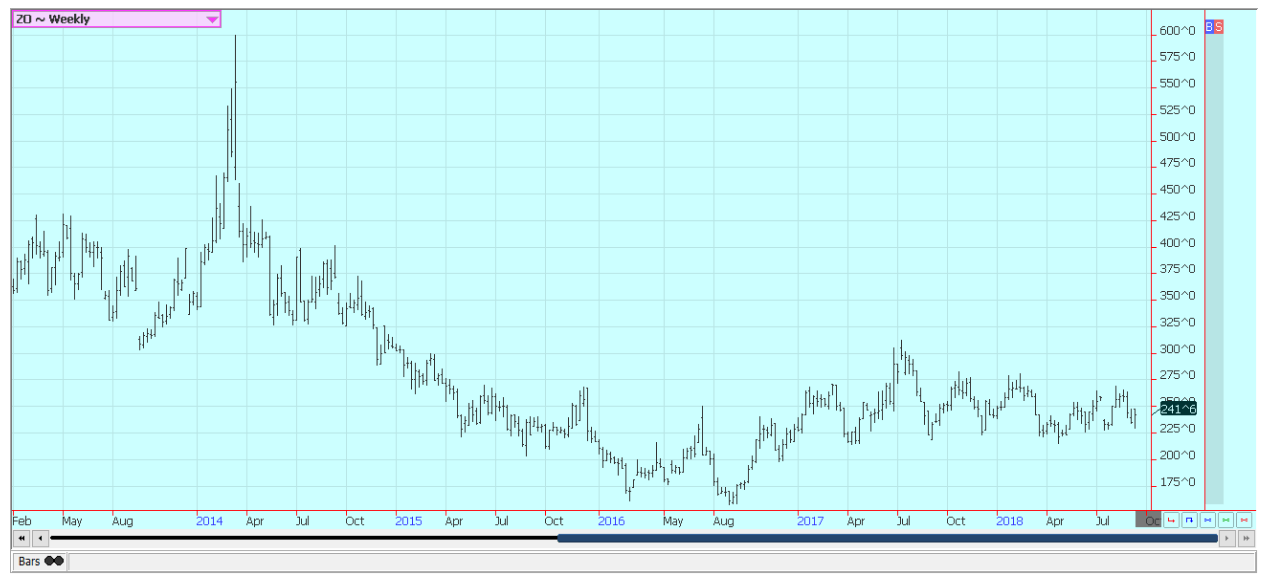

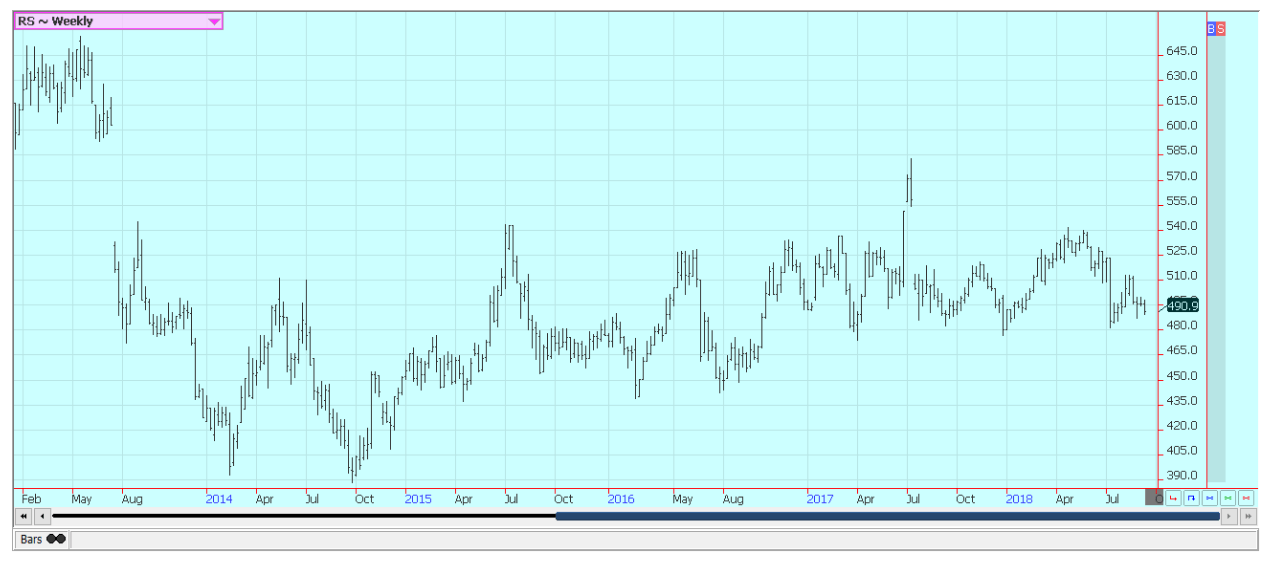

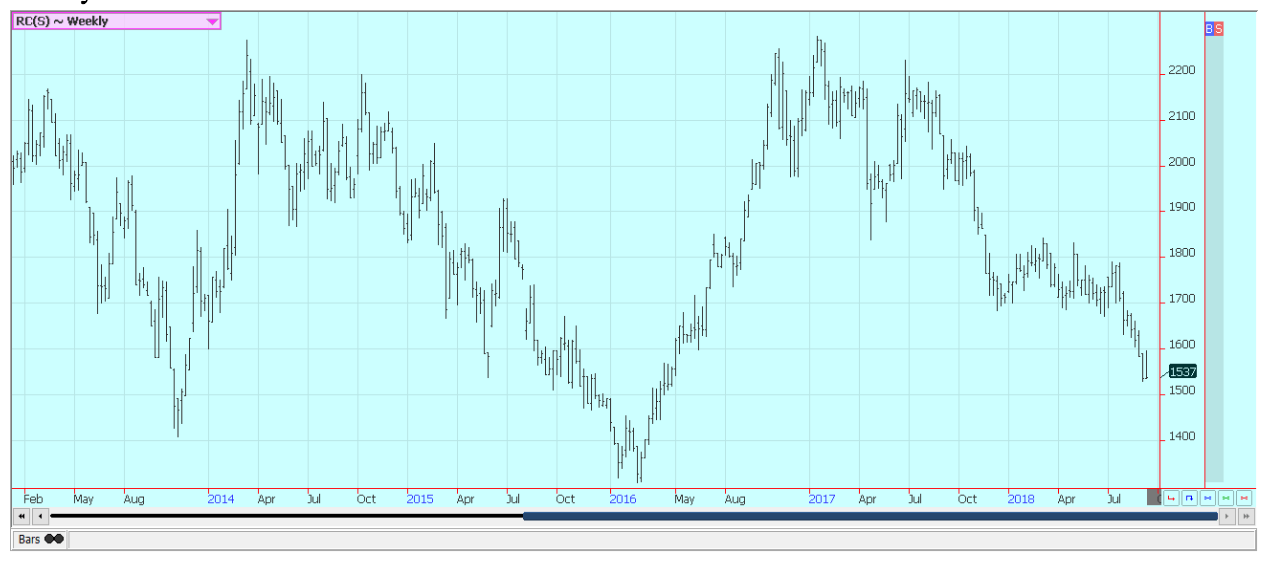

Rice

Rice was lower, with much of the selling developing on Friday. Good to excellent yields have been reported in Texas and Louisiana so far, and the harvest is about done in these areas. Cash prices are stable in the interior and have held well considering the weakness in futures.

However, lower prices were reported last week in Texas as the main buyer has left the market for now. Ideas are that they have bought enough rice to cover commitments at this time. Other storage facilities in the state are full, so farmers will have to store whatever is still left. Milling yields have been acceptable or mostly very good.

The harvest is much more active this week in Mississippi and to the north into Arkansas. The quality should remain strong overall. USDA released its production and supply and demand estimates on Wednesday.

Production of all rice was estimated at 219 million hundredweight, up from 210 million estimated last month. Domestic demand was increased, but export demand was unchanged. Ending stocks were increased to 231 million hundredweight from 229 million in August.

World data also held no real surprises. Ending stocks were increased to 144.4 million tons from 143.5 million in August. Increased production was estimated for India, and it faced increased ending stocks in part from the increased production and in part from bigger carry-in stocks. The Philippines is also expected to have increased ending stocks.

Weekly Chicago Rice Futures © Jack Scoville

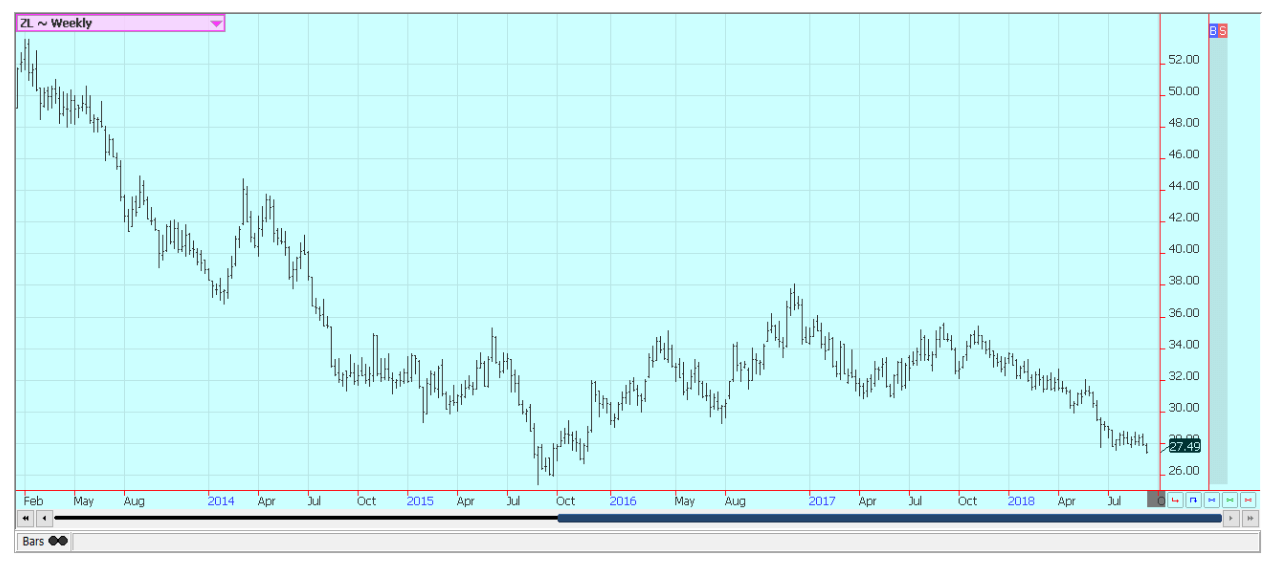

Palm oil and vegetable oils

World vegetable oils prices were mixed last week. Palm oil was a little high on the week as traders reacted to the strong export estimates for the first 10 days in September from the private sources. However, the MPOB monthly export data was poor and bearish for the market. MPOB showed much less demand than anticipated, and production was higher as anticipated.

Ending stocks for the month were much higher than anticipated, and the market sold off in response to the news. Soybean oil was locked in a sideways trend all week and closed lower on some price weakness that developed on Friday. Trends are sideways in the market, but prices could work lower if soybeans stay weaker. Demand for biofuels has been strong, but export sales were nonexistent last week. Canola was lower as the harvest is getting started. Early reports indicate variable and somewhat disappointing yields in the south, but better than expected yields in the north. Ideas are that the recent StatsCan estimates could be too low. Yields have been coming in generally above trade expectations.

Weekly Malaysian Palm Oil Futures © Jack Scoville

Weekly Chicago Soybean Oil Futures © Jack Scoville

Weekly Canola Futures © Jack Scoville

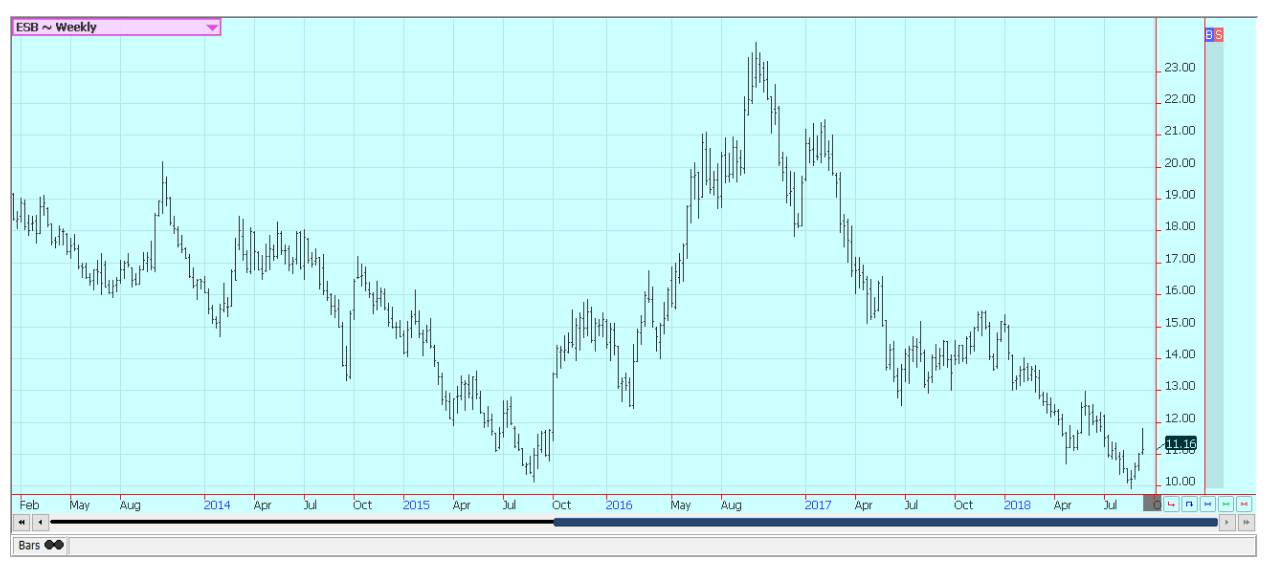

Cotton

Cotton was a little lower for the week in choppy trading. USDA increased production estimates on Wednesday due to the increased area as yields were lower. The trade had expected a slight decrease in production. It also increased exports and forecast only a slight increase in ending stocks despite the increased production.

World data showed few changes. These estimates could be subject to change due to the arrival of Hurricane Florence over the weekend. The storm has caused significant damage and losses to crops from Virginia to Georgia. U.S. weather remains good in the Delta and Southeast away from hurricane areas and has improved slightly in West Texas on north into Kansas with improved precipitation. Even so, the crop is generally in poor condition in much of Texas and there are real questions on just how good the yield can be in the state this year.

The harvest has been active in far southern parts of the state. Crop scout reports indicate that the yield potential should be generally poor. Eastern Texas crops are in good condition and about ready for harvest. Bolls are opening in the Delta and Southeast. The trade is monitoring the weekly Cotton Classings report for clues on yields and also quality. The reports are showing that just over half of the arrivals were tenderable. Classings data has been improving as the harvest starts to expand.

Rains from the Indian monsoon have been below normal but generally good enough to support crops. The trade there remains optimistic that a good crop is coming and that they will not need to import very much cotton this year. China has been active in India buying and will buy as much as possible there to make up for production losses inside of China. Conditions have also improved in Pakistan as rains have been reported.

Weekly US Cotton Futures © Jack Scoville

Frozen concentrated orange juice and citrus

FCOJ was lower last week in range trading as the hurricane season got busier. The summer has been a quiet one in the Atlantic, but all that changed last week as one storm brushed Florida and another slammed into the Carolinas. There are other systems developing that could impact Florida in the next week or so. Chart trends are mixed as the market has found some support from speculators due to the increase in storm activity.

Overall growing conditions in Florida are good to very good, and there is no storm development in the Atlantic at this time. The state is getting frequent periods of showers. Florida producers are seeing good-sized fruit, and work in groves maintenance is active.

Irrigation is being used when needed, and producers expect a good crop. A good crop now will likely mean increasing inventories of frozen concentrate.

Weaker demand has caused FCOJ inventories in Florida to increase on a year to year basis. USDA released production data for the previous crop. Florida oranges production was left unchanged at 45 million boxes and total U.S. production was estimated at 92 million boxes from 90 million estimated in June. Florida FCOJ inventories are now 253 million gallons, up 42 percent from last year.

Weekly FCOJ Futures © Jack Scoville

Coffee

Futures were lower last week in New York, but near unchanged in London. Ideas of strong production in Brazil and Vietnam are keeping futures under selling pressure. Speculators have been looking at the weakness of the Brazilian Real against the US Dollar and have been selling coffee on ideas of increased offers in Brazil.

Vietnam is getting close to its next harvest, and ideas are that producers there need to sell more of the previous crop to create new storage space. Producers in both countries are not selling, although there is a talk of some big sales in Brazil. But, the market is generally quiet there due to the after effects of the truckers strike.

Arabica trees in Brazil were starting to show stress due to the lack of rain over the last few months. It will be dry again for the rest of the week. The months leading up to the winter were also dry, and that early dryness is affecting trees now. It is very possible that some production could be lost for the next crop due to the very dry overall conditions.

Estimates for production this year range as high as 60 million bags. Most of Central America is reporting good rains, so the overall losses could be minimal. Production in Vietnam is estimated at above 30 million bags and a new record. Growing conditions are called good.

Weekly New York Arabica Coffee Futures © Jack Scoville

Weekly London Robusta Coffee Futures © Jack Scoville

Sugar

New York was higher and London was near unchanged last week. New York price action overall is stronger, but both markets saw some big selling on Friday on reports of some very timely showers in Brazil growing areas. Ideas of big world production are bearish and have been the reason for the selling. Just about everyone is looking for a significant production well above any demand potential.

Dry conditions continue in Brazil, the EU, and Russia, but conditions are mostly good in Ukraine. Very good conditions are reported in Thailand and India. Brazil producers are worried about cane production even with the rapid early harvest, and the market is now starting to talk about less production there this year. The dry weather in much of Europe and in southern Russia near the Black Sea has hurt sugarbeets production potential in these areas. Recent rains in parts of Ukraine have continued to improve production prospects there.

Weekly New York World Raw Sugar Futures © Jack Scoville

Weekly London White Sugar Futures © Jack Scoville

Cocoa

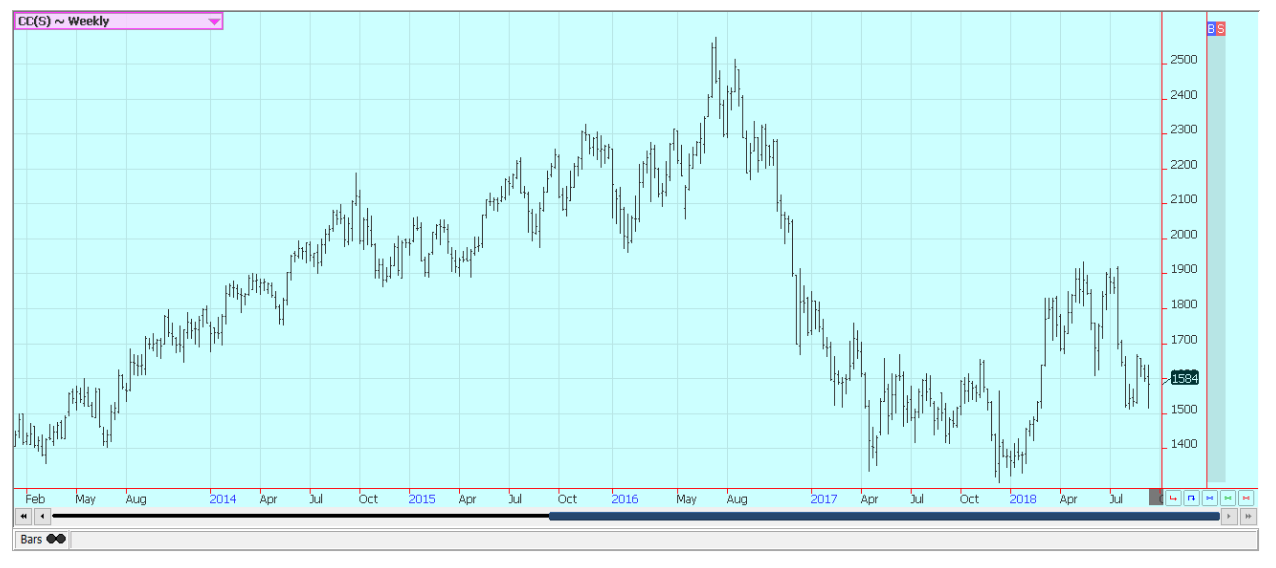

Futures closed lower for the week. The outlook for strong production in the coming year has been enough to keep the prices weak. The main crop harvest is in its earliest stages in some parts of West Africa, but will not really get going for at least another few weeks. Main crop production ideas for Ivory Coast are high. Ghana and Nigeria are expecting very good crops this year as well, although Nigerian estimates have started to drop a little bit on the volume of rains that have hit the country in recent weeks. Conditions also appear good in East Africa and Asia.

Weekly New York Cocoa Futures © Jack Scoville

Weekly London Cocoa Futures © Jack Scoville

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation for writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

The TopRanked.io Guide to 2026’s Biggest and Best Affiliate Opportunities

Want to earn affiliate commissions on literal billions of dollars worth of revenue? Then this week, we've got something special...

Eni Advances Energy Transition with Major Investment and Emissions Cuts

Eni showcased its “Just Transition” report in Rome, highlighting stakeholder collaboration and progress toward decarbonization goals. The company invested over...

The German Fintech Market Shows Resilience and Strong Investment Growth in 2026

Germany’s fintech sector remained resilient in 2026 despite economic crisis and rising insolvencies. Investments reached €14.2 billion, showing strong investor...

Cannabis Legalization in Germany: A Mixed Interim Assessment

Germany’s cannabis legalization has reduced criminal cases and eased pressure on the justice system, while the black market is slowly...

Sustainable Restoration of the Haus Hövener Garden in Brilon

The Brilon Construction Workers Association is restoring the Haus Hövener garden into a cultural community space, funded through a €10,000...

|

|

|  |

|

|

-

Biotech5 days ago

Biotech5 days agoTG Therapeutics Advances Subcutaneous Briumvi With Strong Trial Results and Rising Sales Momentum

-

Crypto2 weeks ago

Crypto2 weeks agoAltcoins Show Mixed Performance as Bitcoin Weakens

-

Fintech3 days ago

Fintech3 days agoTemenos to Acquire Additiv to Boost AI Wealth Management

-

Cannabis1 week ago

Cannabis1 week agoAmsterdam Keeps Coffeeshops Open to Tourists While Raising Europe’s Highest Tourist Tax

You must be logged in to post a comment Login