Business

Cocoa market concluded the past week on a sour note as futures dropped

Aside from cocoa, the soybean and soybean meal market also experienced a decrease last week.

The cocoa market experienced a slight decline in its futures last week. However, cocoa prices remain steadfast thanks to strong demand.

Wheat

US markets closed slightly higher last week but gave back most of the weekly rally late in the week as the US Dollar turned higher and due to a disappointing export sales report released on Thursday by USDA. Overall export demand has been about as projected by USDA, but ideas of ample supplies and strong competition from Russia keep futures pinned at cheaper levels. However, prices should have limited downside potential and should be able to trend a little higher over time. There are production problems around the world apart from Russia this year.

Ukraine and Australia have reported smaller crops, and the excessive rains in southern Brazil and Argentina have hurt crops in those countries. The Brazilian government has moved to allow the duty-free import of up to 7.0 million tons of wheat this year, with about 4.0 million expected to be sourced from producers other than Argentina. The US looks to plant fewer acres to wheat again this year, meaning that the US will have less area planted to wheat than seen over the last 100 or more years once again this year.

However, the market remains fixed on the strong competition and low prices offered from Russia. Russia is looking to maintain its dominant position in the world market and is hoping to raise another huge crop this year. The next crop of winter wheat is getting planted now. It is also working hard to expand and improve its logistical infrastructure, although it will take some time to see the full effects of that investment. It is close to major buyers in Africa and the Middle East, and that is a natural advantage in freight costs. Ideas are that Wheat prices can remain a sideways and choppy trade for now.

Weekly Chicago Soft Red Winter Wheat Futures © Jack Scoville

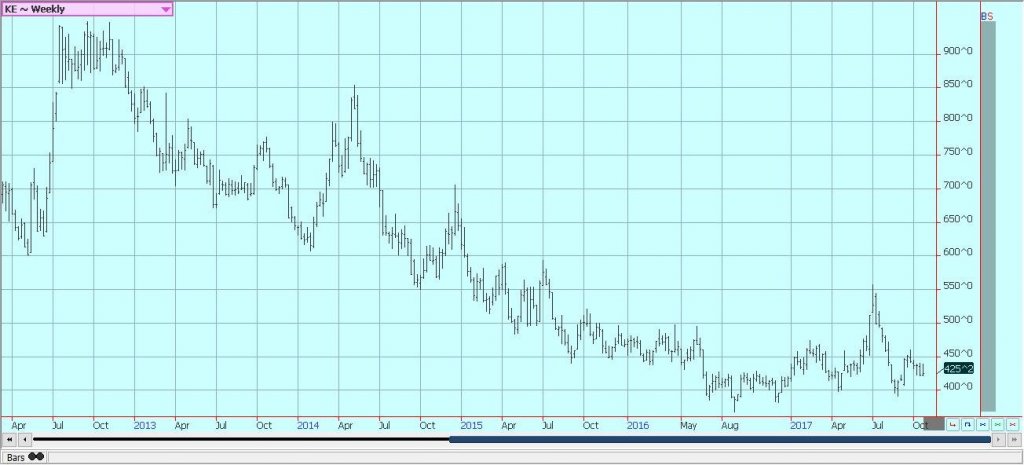

Weekly Chicago Hard Red Winter Wheat Futures © Jack Scoville

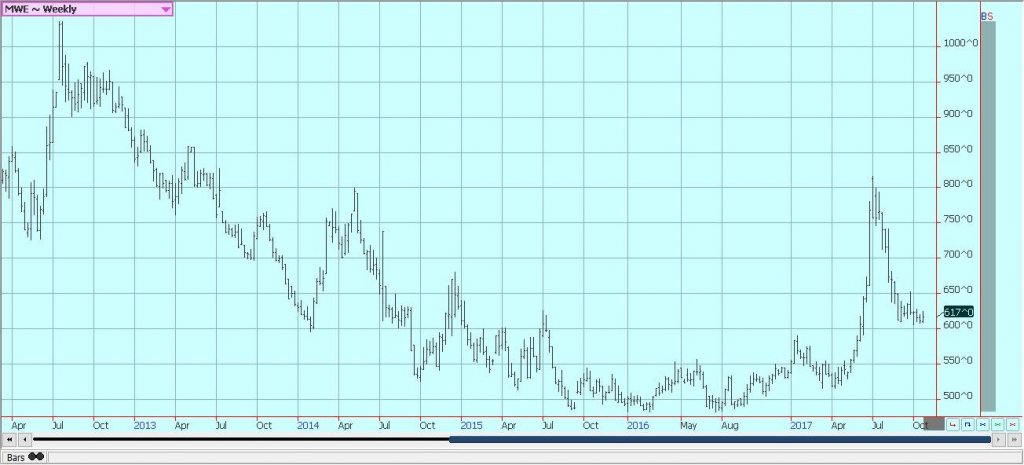

Weekly Minneapolis Hard Red Spring Wheat Futures © Jack Scoville

Corn

Corn closed slightly higher and oats closed a little lower for the week as the US corn harvest expands in much of the Midwest. Oats closed lower after making new highs for the move. Ideas are that the corn crop can be over 60% harvested when USDA releases its weekly progress reports on Monday afternoon. The export sales report on Thursday was very strong for Corn and was a reason to buy the market, but the US Dollar moved sharply higher in reaction to the economic news here and in Europe. The dollar moves negated the strong demand in the trade action.

Basis levels remain generally weak but have continued to improve as the market starts to need some corn. There has been talk of active demand from ethanol producers who waited to see what EPA would do to modify production mandates. EPA has announced that it will not seek to lower production mandates and this has helped demand ideas for the big crop. The market is hearing more harvest results as activity moves north and west.

Yields have been generally strong, but the harvest pace has been a little slow as producers have been concentrating more on getting the soybeans harvested and letting the corn dry in the fields. Many producers in central and eastern areas are now about done with the soybeans harvest and will now concentrate on corn. Producers in Minnesota and parts of Wisconsin saw a storm last week that brought rain and snow and some very strong winds. Ideas are that there could be some yield loss, but nowhere near enough loss to change the fundamental situation of comfortable supplies. Corn futures could remain a sideways and choppy trade for now.

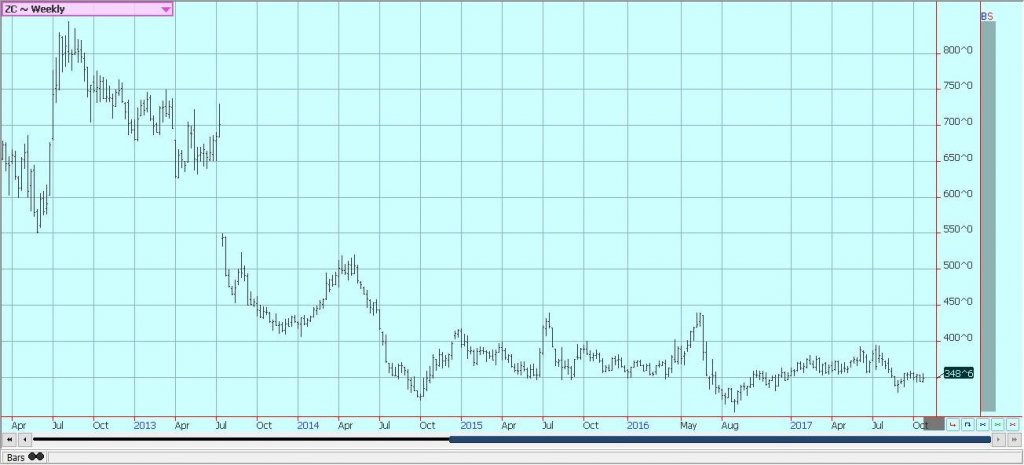

Weekly Corn Futures © Jack Scoville

Weekly Oats Futures © Jack Scoville

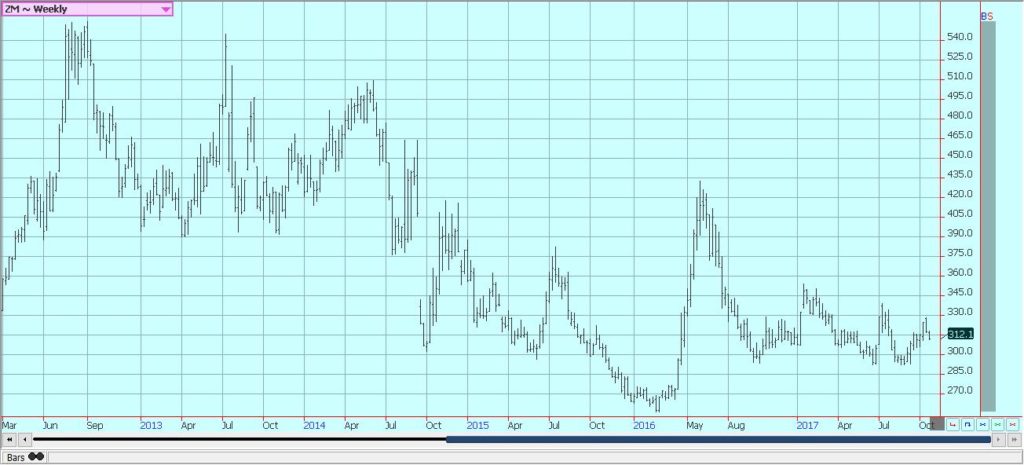

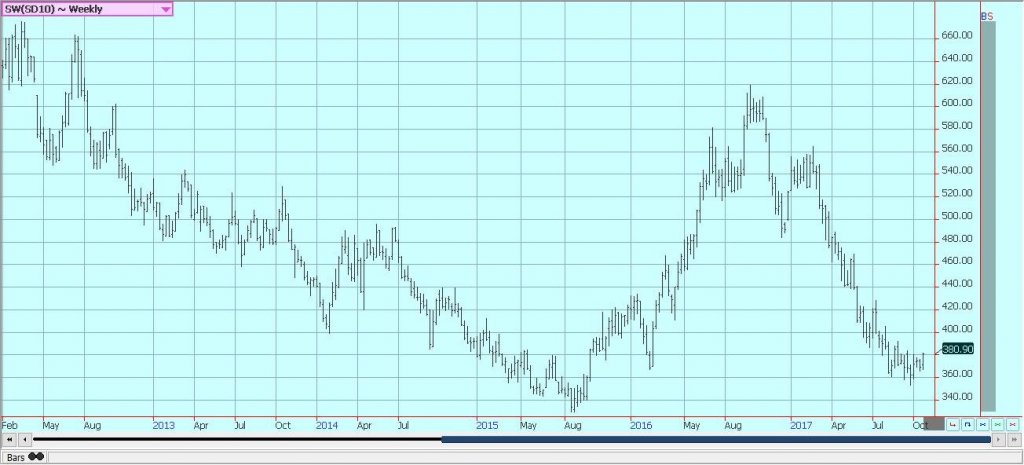

Soybeans and Soybean Meal

Soybeans and soybean meal were a little lower last week as the US Dollar moved sharply higher in response to economic news from Europe and the US. The dollar moves negated the strong weekly export sales report that showed China returning to the US market. The Chinese demand now is welcome as it had been sourcing almost all of its soybeans needs from Brazil. Soybean meal also suffers from weak demand due to strong competition from DDGS in the market and on ideas that crush levels can remain strong due to the need to produce soybean oil for biofuels needs.

Harvest weather should be good this week in the Midwest after weekend rains as forecasts call for cool and dry conditions. There are still forecasts around for weather patterns to change in Brazil and bring some badly needed rain to the north and drier conditions to the south and into Argentina. Some beneficial rains have been reported in Mato Grosso and Mato Grosso do Sul but have missed the Mapito region. It remains too wet to the south.

The US harvest is now about over in areas east of the Mississippi River, while areas to the west of the river are moving quickly to get done. The yield data generally runs behind year-ago levels, but are still very strong overall. Basis levels have started to improve in the interior as the harvest selling winds down, although basis levels have been weak in the Gulf of Mexico. Soybeans are still holding an uptrend that started in mid-August but has found significant selling on rallies above $10.00 per bushel.

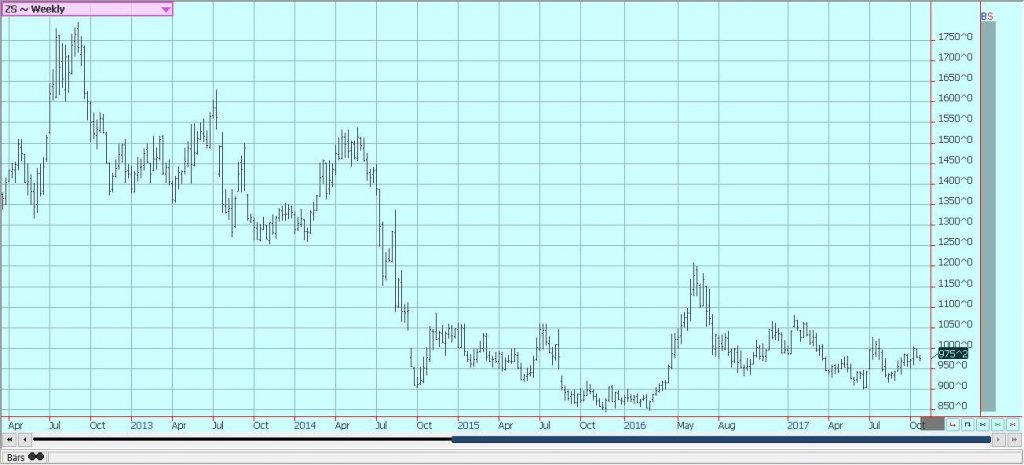

Weekly Chicago Soybeans Futures © Jack Scoville

Weekly Chicago Soybean Meal Futures © Jack Scoville

Rice

Rice closed higher on Friday, but lower for the week. The daily and weekly charts both show downtrends, and the weekly charts imply that moves to about 1110 November are possible. The sales report last week was strong and were especially strong for long grain into Latin America. It was the strongest weekly sales report of the year so far and shows that demand for good quality US rice is improving. That demand news has been great for the market. Latin American buyers in recent years have complained about the quality of the US crop and have bought more and more from Brazil or elsewhere in Latin America.

The strong sales now show that the US quality is very good this year and also that the US is featuring competitive prices into these regions. Domestic cash market conditions are generally quiet with stable flat price bids. The Delta harvest is over and as farmers are holding out for higher prices. Reports from the country indicate good to very good yields and quality. Yields in California right now are lower than hoped for as that harvest winds down. Domestic cash quotes have held generally steady in California.

Weekly Chicago Rice Futures © Jack Scoville

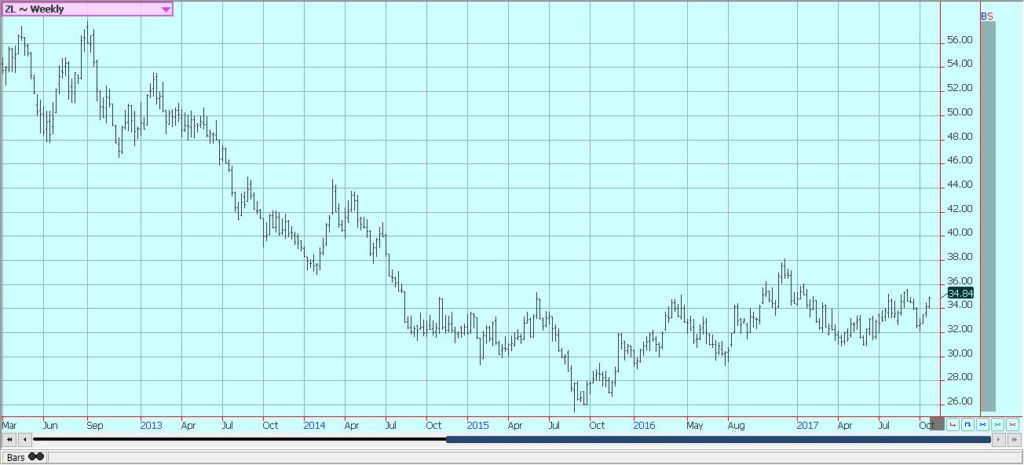

Palm Oil and Vegetable Oils

Palm oil futures moved a little higher once again last week, and weekly charts show that the market remains in a trading range. The market moved higher as data released by the private sources showed that exports for most of the month were very strong. Both showed that exports this month are at least 10 percent higher than last month, and this strong demand has held together for each reporting period. The strong demand went against ideas of weakening demand due to the end of the Chinese holidays and has been a surprise to the market. China is back and buying now and demand could get stronger.

Canola was higher on a much weaker Canadian Dollar and on decreased farm selling as the harvest starts to come to a close. Yield reports yet imply a good but not great crop in just about all areas of the Prairies. Soybean oil was also higher. Ideas are that US domestic Soybean Oil demand can stay strong for biofuels. World vegetable oils markets continue to be as strong as any in the agricultural world and the fundamentals of good demand would seem to indicate that generally strong prices can continue.

Weekly Malaysian Palm Oil Futures © Jack Scoville

Weekly Chicago Soybean Oil Futures © Jack Scoville

Weekly Canola Futures © Jack Scoville

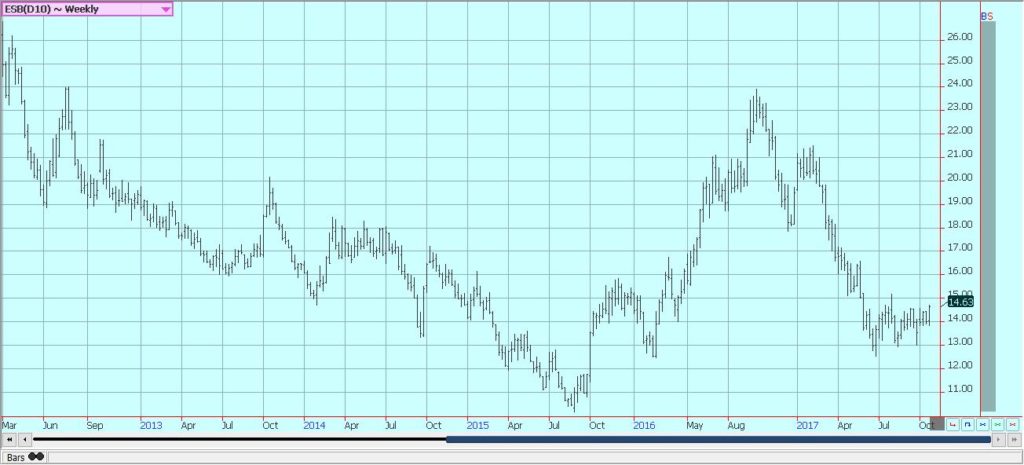

Cotton

Cotton was higher for the day and higher for the week. It was a midrange close for the week as traders factored in the potential for a freeze in the Texas Panhandle over the weekend and also waited to see the effects of the Indian government move to increase support prices for cotton producers. The moves in India are widely viewed as an attempt to shore up the farm vote by the ruling party as elections are coming next month.

The Indian subsidies will be higher than trade expectations and ideas are that the US could see new demand due to higher Indian prices that will need to be charged now. A freeze in Texas could cause the loss of about half a million bales. Even so, production would be very large. A sharply higher US Dollar late last week hurt the rally attempt as there is a lot of cotton to sell and the sharp rally hurt demand ideas in a big way.

The Texas weather could get cold enough to freeze the crops and some cotton could be lost. Mature cotton would not be affected, but green bolls would be damaged and lost. The harvest ahead seems to be the most important factor as USDA is expecting a huge crop. Bolls are opening and harvest is expanding under relatively good conditions as it has been relatively dry. Good harvest weather is expected this week.

Weekly US Cotton Futures © Jack Scoville

Frozen Concentrated Orange Juice and Citrus

FCOJ closed higher and appears to be in a new trading range. The market has not been able to fill a gap left in reaction to Irma and the losses seen in Florida as a result of the devastating storm. Futures are still reacting to t the USDA reports that showed big production loss potential from the hurricane, but not the losses expected by the trade. USDA is expected by many to show further dramatic cuts in production in coming reports. USDA will have more time to do a complete survey.

It is expected that as it learns more about the damage, USDA will be able to drop production estimates even more than it has. It should find that crops in many areas were almost completely destroyed. Other areas suffered losses of 50% or more of the crop. Some growers say that trees will be stressed again next year due to the winds and rains from Irma. The demand side remains weak and there are plenty of supplies in the US. Trees that are still alive now are showing fruits of good sizes, although many have lost a lot of the fruit. Florida producers are actively harvesting what is left. The emphasis is on the fresh fruit market now, with processors only getting packinghouse eliminations at this time. Brazil crops are stressed from the hot and dry weather.

Weekly FCOJ Futures © Jack Scoville

Coffee

Futures were a little higher in New York and a little lower in London last week, with commercials, scale down buyers and speculators still the best sellers in New York, but now on both sides of the market. The trends are down on the charts in New York as traders look at the potential for a big crop in Brazil. London trends are sideways. The Brazil weather and tree condition is the main fundamental reason for movement in New York prices and could become the major reason to buy the market soon.

Rains have come to coffee areas in Minas Gerais again, but rain amounts have been very light and coverage has been poor. Earlier rains promoted flowering, and some reports indicate that flowering has been very good. These rains were needed for secondary flowering and to maintain tree condition and to help prevent aborting of the flowers. The rains will need to continue and be in good amounts as it has been very dry and trees have been stressed for a year or more in some cases.

Some were stressed after the production last year, while others suffered due to the dry and cold winter. Even so, improved weather now could mean a very good crop, although most likely not a huge crop of over 50 million bags. Cash market conditions in Central America are more active as the harvest continues. Differentials have been stable but weak in the region. Colombian exports have held well as production appears to be good. Differentials have been stable and relatively strong.

Weekly New York Arabica Coffee Futures © Jack Scoville

Weekly London Robusta Coffee Futures © Jack Scoville

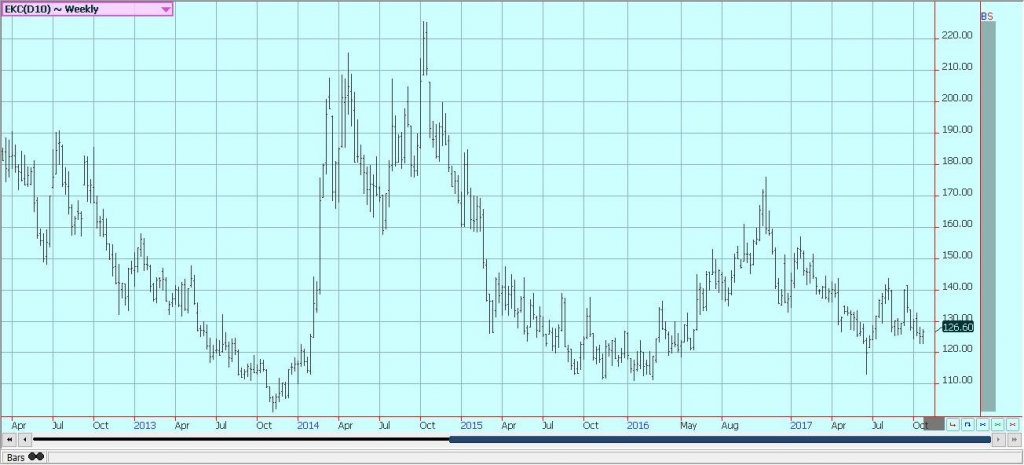

Sugar

Futures were higher and short-term trends in New York turned up as March cleared some resistance just above 1450 on the charts. The market is rallying as UNICA showed reduced production of sugar as mills in Brazil decided to make more ethanol. The move by Brazil mills to produce more ethanol means less sugar available for the world market. Weekly charts show trading ranges. Traders remain generally bearish on ideas of strong world production and lackluster demand.

There does not seem to be any big demand coming from any real direction, especially as China has cut back on imports and the year to year loss in demand is a very big amount. The fundamental side of the market remains mostly negative due to ideas of big world production. Brazil has turned dry after recent rains, and more rain is needed after the dry winter. Some showers could appear early this week. Upside price potential is limited as there are still projections for a surplus in the world production, and these projections for the surplus seem to be bigger.

Weekly New York World Raw Sugar Futures © Jack Scoville

Weekly London White Sugar Futures © Jack Scoville

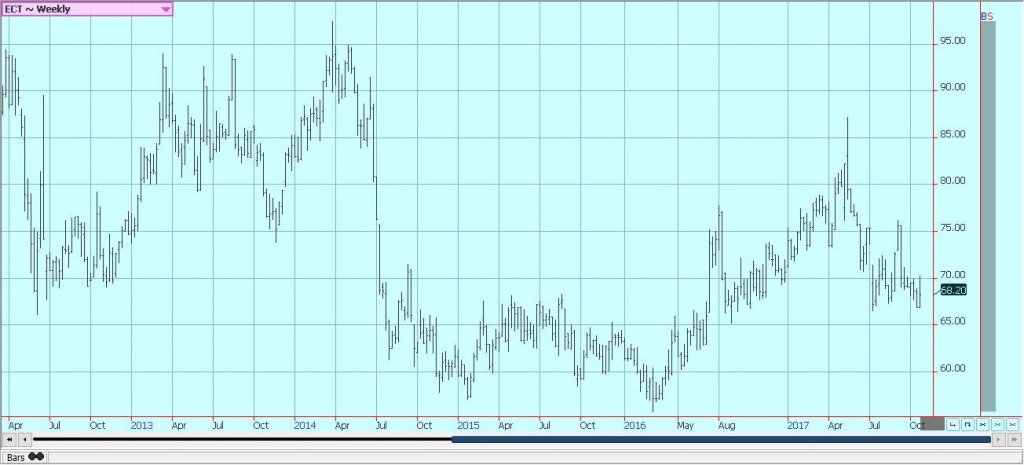

Cocoa

Futures closed a little lower on Friday and a little lower for the week as New York futures faded from resistance near 3360 on the weekly charts. Prices remain strong overall in response to positive demand news from as the North American and the European grind data released earlier this month. The North American data did show an increase in demand, but not as much as some traders had hoped for. The trends are now up in New York and in London on both the daily and weekly charts.

World production ideas remain high. Harvest reports show good to very good production will be seen this year in West Africa. Ghana and Ivory Coast expects a very good crop this year. Nigeria and Cameroon are reporting good yields on the initial harvest, and also good quality. The growing conditions in other parts of the world are generally good. East Africa is getting better rains now. Good conditions are still seen in Southeast Asia. Traders talk of increased demand to go against big world production as prices are now attractive for grinders and chocolate manufacturers.

Weekly New York Cocoa Futures © Jack Scoville

Weekly London Cocoa Futures © Jack Scoville

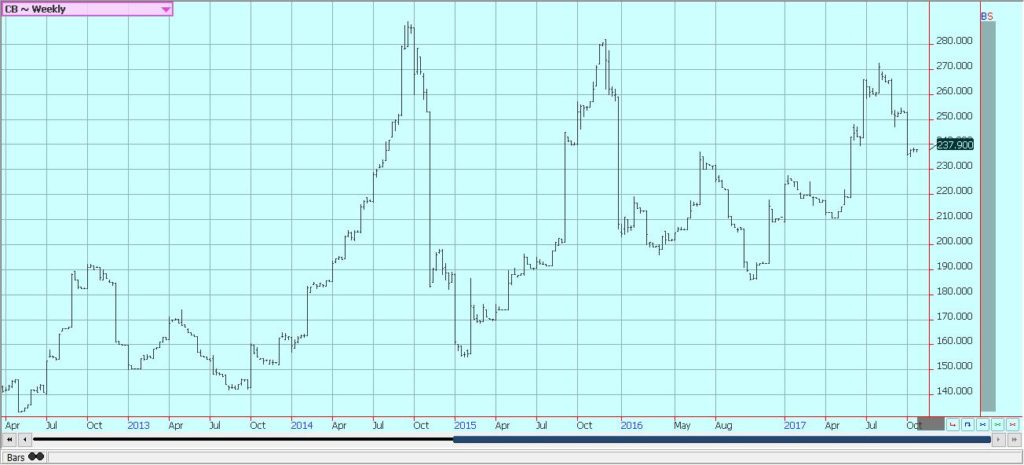

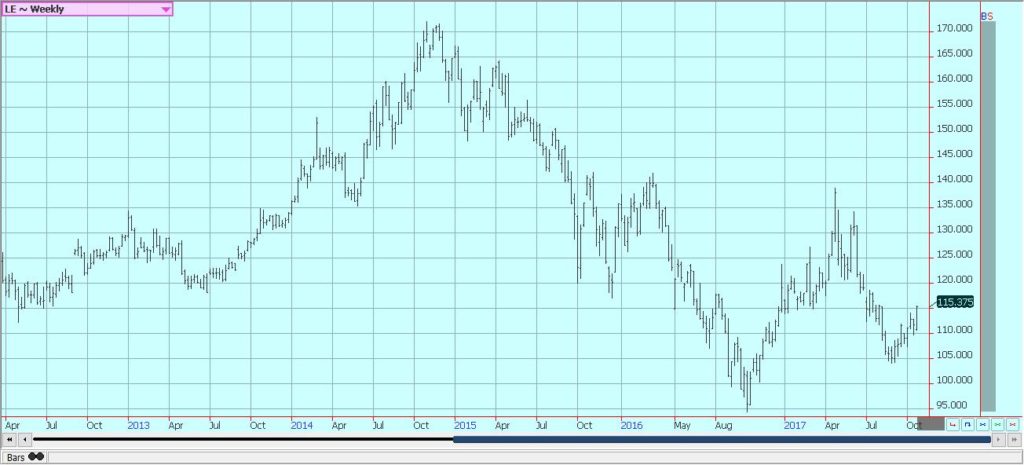

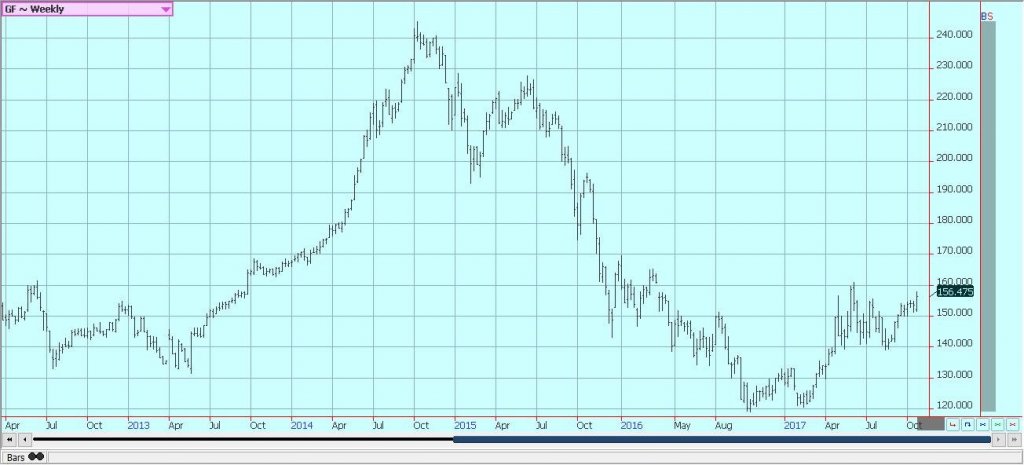

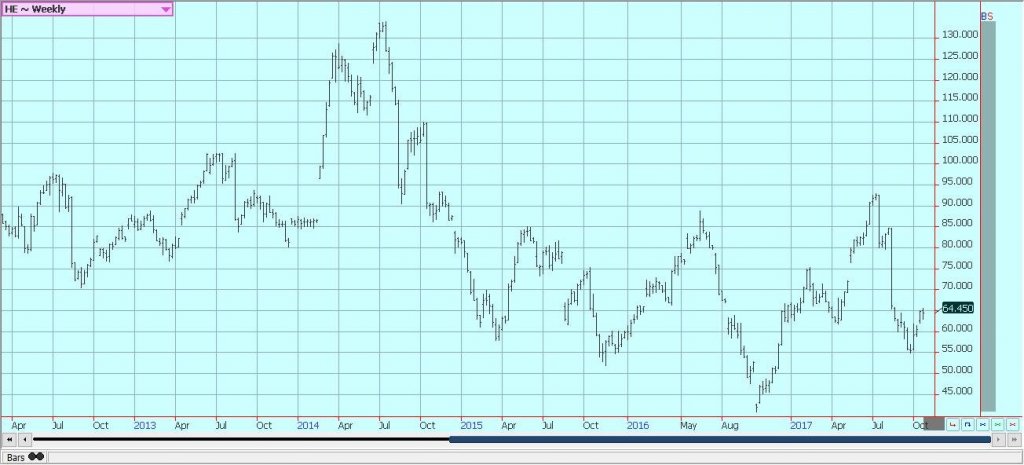

Dairy and Meat

Dairy markets were sharply lower again last week and Milk futures made new lows for the move. The Global Dairy Auction was weaker last week. USDA reports ample supplies, but good to very good demand in just about all parts of the US. Milk and cheese demand has been mixed, but Butter demand has weakened and prices in this market have moved sharply lower. Demand is good for cream, but cream has generally been available to meet the demand.

Cream demand for butter has been very good. Demand for ice cream has been mixed depending on the region but is holding well due to mild weather in much of the US. Cheese demand still appears to be weaker and inventories appear high. US production conditions have featured some abnormally hot weather in the west that is hurting milk production. Production in the rest of the country has been strong.

US cattle and beef prices were lower, but futures held uptrends. Beef prices remain firm, and cattle traded about #2.00 per hundredweight higher last week. Ideas are that packers are still enjoying very strong margins at this time and can afford to pay more for cattle. This did happen last week. The beef market was somewhat better last week to support ideas that prices for cattle could continue to improve.

Cattle prices were steady to slightly weaker in early dealings and amid lighter than expected volume. It is the threat of increased supplies down the road that keeps the packers from buying aggressively. Feedlots are full, but ideas are that the big offer of cattle has passed. The monthly Cattle on Feed report on Friday showed big placements, so prices should move lower this week in both live cattle and feeder cattle futures.

Pork markets and lean hogs futures were higher. Ideas are that futures are reflecting the weaker supply and demand fundamentals now, but the overall market seems to be improving. Demand has been improved for the last couple of weeks and this has affected pricing. There are still ideas of bug supplies out there, but the market seems to have the supply side priced. The weekly charts show that the market is trying to form a low at current prices, and futures have been cheap enough that a low is possible at this time. The weekly charts suggest that futures are completing an important bottom in prices at this time.

Weekly Chicago Class 3 Milk Futures © Jack Scoville

Weekly Chicago Cheese Futures © Jack Scoville

Weekly Chicago Butter Futures © Jack Scoville

Weekly Chicago Live Cattle Futures © Jack Scoville

Weekly Feeder Cattle Futures © Jack Scoville

Weekly Chicago Lean Hog Futures © Jack Scoville

—

DISCLAIMER: This article expresses my own ideas and opinions. Any information I have shared are from sources that I believe to be reliable and accurate. I did not receive any financial compensation in writing this post, nor do I own any shares in any company I’ve mentioned. I encourage any reader to do their own diligent research first before making any investment decisions.

The TopRanked.io Guide to 2026’s Biggest and Best Affiliate Opportunities

Want to earn affiliate commissions on literal billions of dollars worth of revenue? Then this week, we've got something special...

Eni Advances Energy Transition with Major Investment and Emissions Cuts

Eni showcased its “Just Transition” report in Rome, highlighting stakeholder collaboration and progress toward decarbonization goals. The company invested over...

The German Fintech Market Shows Resilience and Strong Investment Growth in 2026

Germany’s fintech sector remained resilient in 2026 despite economic crisis and rising insolvencies. Investments reached €14.2 billion, showing strong investor...

Cannabis Legalization in Germany: A Mixed Interim Assessment

Germany’s cannabis legalization has reduced criminal cases and eased pressure on the justice system, while the black market is slowly...

Sustainable Restoration of the Haus Hövener Garden in Brilon

The Brilon Construction Workers Association is restoring the Haus Hövener garden into a cultural community space, funded through a €10,000...

|

|

|  |

|

|

-

Africa2 weeks ago

Africa2 weeks agoBank of Africa Leads Winners at African Banker Awards

-

Impact Investing3 days ago

Impact Investing3 days agoTransition to a Sustainable Economy as a Strategic Global Shift in a Fragmented World

-

Cannabis1 week ago

Cannabis1 week agoTilray Expands in Europe as Medical Cannabis Market Grows

-

Impact Investing22 hours ago

Impact Investing22 hours agoEni Advances Energy Transition with Major Investment and Emissions Cuts

You must be logged in to post a comment Login