Featured

The world is slowly recovering from the Coronavirus scare

Cotton was higher last week and closed above the previous weekly low. Support is coming from hopes and ideas of improved demand for US Cotton. The weekly export sales report showed a modest increase in sales after a couple of weeks of big net cancellations. The world is starting to slowly recover from the Coronavirus scare and some stores are starting to open again after being closed for weeks.

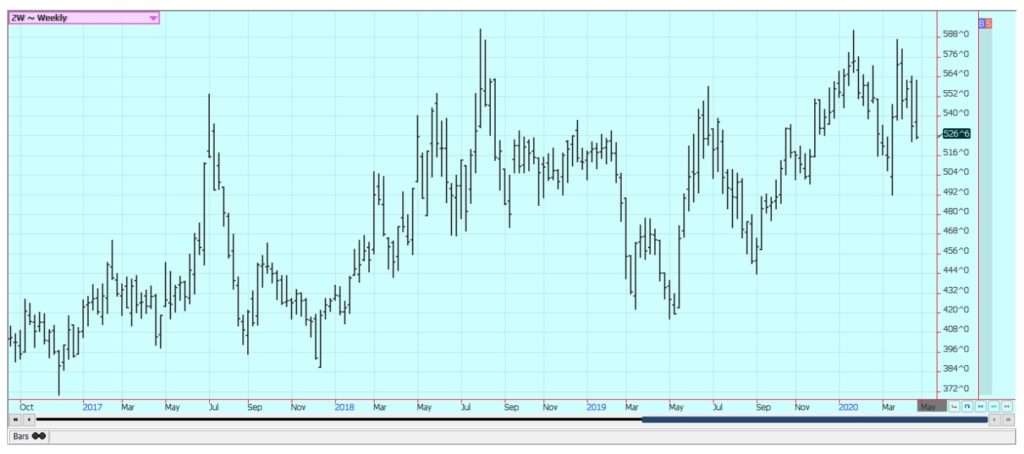

Wheat

Wheat markets were lower for the week but held the previous week’s range. World cash markets, in general, are much cheaper than those prices offered from the US. That will help keep any US export sales low and routine. US domestic demand has softened after a surge higher about a month ago due to stocking at the start of the Coronavirus outbreak. The world weather is important for new crop prices. US weather has been wet in the central and southern Great Plains and very wet in southern and eastern sections of the Midwest as well as the Midsouth, Delta, and Southeast. It has been dry in the northern Great Plains and into the Canadian Prairies. Europe has also been dry but was expected to get some very beneficial rains this week. It remains dry in Ukraine and into southern Russia. Australia is in mostly good condition after several years of drought. Argentina is still harvesting its Corn and Soybeans crops and has not really planted its Winter Wheat crop yet.

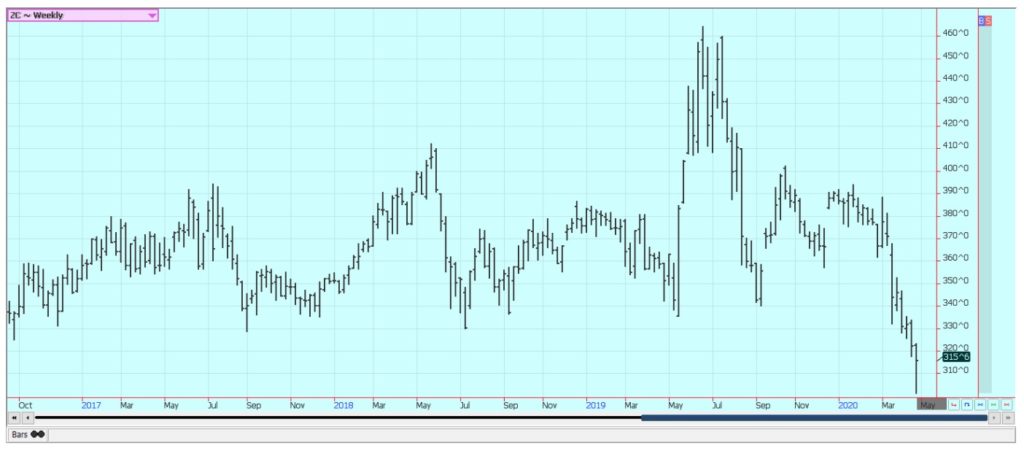

Corn

Corn was lower and May Corn traded near the 300 level for the first time in many years last week. The market was able to recover somewhat from that level and it is possible that futures have seen at least a short term low. The main fundamental remains demand destruction caused by the ack of ethanol demand and the lack of feed demand. Both have been detrimentally affected by the Coronavirus that has affected so many areas of life around the world. The virus has caused states to impose stay at home orders on its people, meaning no one is driving and consuming gas. Even the news that Russia and Saudi Arabia found a truce and that world Crude Oil production would be 10 million barrels a day less did little for the market as consumption is down by 20 million barrels per day. Some states are starting to open now in the US but it is unclear if the people will move out and enjoy life as before. The experience in other countries suggests that the people will be very cautious in any activities and really not go out and spend money or hit the stores as before. Driving will be significantly less either way. Feed demand has been reduced as packers have been forced to shut [plants down due to infected employees in the plants. Wholesale beef and pork prices are up sharply, but cattle and hog producers are seeing very cheap prices and are liquidating herds. The Corn demand has been significantly reduced.

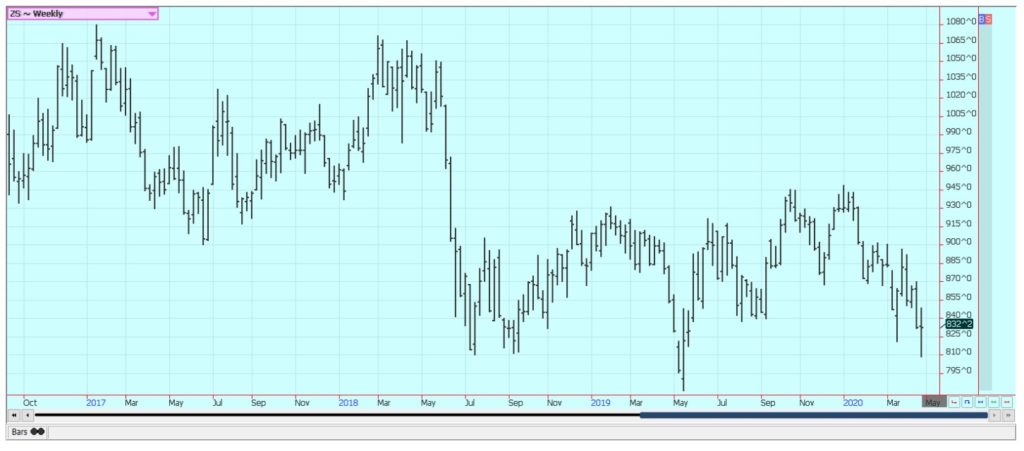

Soybeans and Soybean Meal

Soybeans and Soybean Meal closed a little lower last week after moving sharply lower. Soybeans found support after some significant purchases from China. China used the break in prices to buy at least half a million tons of US old crop Soybeans and possibly more. The news buoyed a market in search of demand. The demand has been slow otherwise with the significant competition from Brazil. The Real has weakened a lot against the US Dollar and Brazil producers can sell at very high prices in the local currency. Meanwhile, soybean Meal demand has been supported by logistical issues in Argentina. The Parana River has been very low and ships are not able to load the full amount of Soybeans or products. Demand has shifted to the US and also to Brazil. Some forecasts for improving rains in southern Brazil and northern Argentina offer hope for improved logistics in the coming weeks. The export meal demand has helped keep the US crush very strong. Domestic meal demand has suffered along with the demand for Corn due to reduced feed demand caused by the Coronavirus and the problems it has caused feed operations.

Rice

Rice was sharply higher in old-crop months and lower in new crop months. The domestic situation remains tight. Some producers are selling the next crop and some significant hedge selling has been seen in new crop months in futures but this has dried up as Arkansas has been cool and wet for planting. Planting was active last week in the state but has been shut down again in southern areas. Demand for US Rice remains generally positive and the export sales pace, in general, has been very good. Mills and exporters are calling previously bought Rice to keep the market supplied. This is happening mostly in Arkansas as Gulf Coastal areas are mostly sold out of Rice. The weekly crop progress reports showed that southern Rice is emerging well. Arkansas should get a window to plant next week. Mississippi needs drier weather.

Palm Oil and Vegetable Oils

Palm Oil and Soybean Oil were sharply lower last week, but Canola held and closed close to unchanged. Palm Oil and Soybean Oil were hurt by the lack of bio fuels demand. The same factors affecting ethanol demand are affecting demand for other bio fuels. People are driving less due to the Coronavirus and even reduced Crude Oil production has not been enough to lift prices to profitable levels for bio fuels producers. Palm Oil had found some support from reduced production potential in Southeast Asia as workers are affected by the virus, but the support proved to be fleeting. Meanwhile, Canola has found support from the recent recovery in Soybeans along with a weaker Canadian Dollar. Canola is more of a food oil than the others, although it also has bio fuels uses. China has recently allowed Canadian Canola imports to resume, so demand could soon improve.

Cotton

Cotton was higher last week and closed above the previous weekly low. Support is coming from hopes and ideas of improved demand for US Cotton. The weekly export sales report showed a modest increase in sales after a couple of weeks of big net cancellations. The world is starting to slowly recover from the Coronavirus scare and some stores are starting to open again after being closed for weeks. The hope is that consumer demand for Cotton products will quickly return, but this is not likely to be the case. Consumers have really been hurt economically due to stay at home orders imposed here and overseas and it will take some time for them to recover. As an example, Chinese stores have been open for several weeks but there has been no consumer rush to go to them and buy.

Frozen Concentrated Orange Juice and Citrus

FCOJ was a little higher on Friday and higher for the week. Trends have turned up in the market again after retrenching between 105 and 110 basis May futures. Support is coming from the continued effects from the Coronavirus that are keeping people at home and drinking Orange Juice in any form. Demand from grocery stores has remained strong in response to the increased consumer demand. Nielsen said last week that consumer demand had risen 45.6% in the four weeks ending April 11 to 11.44 million gallons. The average price was the highest in at least two years at $7.23 per gallon. Oranges production was estimated as less in the latest USDA reports at 70.4 million boxes, so supplies available to the market are somewhat reduced. Inventories in cold storage remain solid so there will be FCOJ to meet the demand. The weather in Florida has become a mixed bag over the last few weeks. It has been very hot and dry in south Florida but the north has gotten a lot of rain. The midseason Oranges harvest is diminishing. Irrigation has been run several times per week in most areas. Color break is reported on late variety Oranges. More signs of early bloom and new growth on trees are reported. Favorable weather is reported in Brazil.

Coffee

Futures were lower in both markets last week. New York took a big hit lower on Friday in the face of depressed consumer and roaster demand in the US and Europe. The demand from coffee shops and other foodservice operations has dropped to almost nothing. Consumers are still drinking coffee at home, but many smaller roasters are actively trying to unload green coffee already bought as there are no outlets for sales at this time. The logistics of moving Coffee from Central and South America remain difficult. Producers have had trouble getting workers to pick the cherries and mills and processors have had trouble getting workers to staff the plants. Shipping logistics have improved somewhat, but many are still having trouble getting the Coffee to ports to move to consumer nations.

Sugar

New York and London closed lower and trends remain down. The recently weaker petroleum futures make higher-priced ethanol that much more expensive to blend and cut demand. Prices in petroleum futures remained generally firm last week but still have a long way to go before Ethanol processing becomes profitable again. That makes more Sugarcane available for processing into Sugar. The Brazil mills are trying to cover the lack of White Sugar in the market and the price action suggests that they are succeeding. Reports indicate that little is on offer from India. Thailand might also have less this year due to reduced planted area and erratic rains during the monsoon season.

Cocoa

New York and London closed lower on Friday, but higher for the week on news that the Ivory Coast President and Secretary-General had contracted the Coronavirus. The virus has made it to West Africa and has greatly complicated farming and marketing efforts. Ideas are that deliveries can be slower on any contracted Cocoa and that the next crop could suffer as workers stay away. Analysts interviewed by Bloomberg News estimated the grind in Europe and North America moderately lower. The Coronavirus helps keep demand away and helps keep workers from grinding facilities and chocolate manufacturers. Harvest is now over for the main crop in West Africa and the results so far are very good. Ideas are that demand is less than before due to the Coronavirus problems in Europe. The reports from West Africa imply that a big harvest in the region. The weather in Ivory Coast is good. The weather is too dry in Ghana and Nigeria and there are fears that the mid crop is not developing well at this time.

—

(Featured image by Virgil Cayasa via Unsplash)

DISCLAIMER: This article was written by a third party contributor and does not reflect the opinion of Born2Invest, its management, staff or its associates. Please review our disclaimer for more information.

This article may include forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “estimate,” “become,” “plan,” “will,” and similar expressions. These forward-looking statements involve known and unknown risks as well as uncertainties, including those discussed in the following cautionary statements and elsewhere in this article and on this site. Although the Company may believe that its expectations are based on reasonable assumptions, the actual results that the Company may achieve may differ materially from any forward-looking statements, which reflect the opinions of the management of the Company only as of the date hereof. Additionally, please make sure to read these important disclosures

Bank Al-Maghrib Launches Reforms to Boost Credit via Non-Performing Loan Market

Bank Al-Maghrib is advancing a secondary market for non-performing loans to free bank financing and boost credit. With Moroccan NPLs...

Cyberpunk Trading Card Game Surges Past Goals on Kickstarter

The Cyberpunk Trading Card Game crowdfunding campaign has seen massive success, quickly surpassing its initial goal and raising over 12...

Aurora Shifts Strategy Toward Global Medical Cannabis Markets

In March 2026, Aurora exited the recreational cannabis market to focus on higher-margin global medical cannabis. With 81% of revenue...

SPECT-CT: Advanced Imaging for Precise Cardiac Assessment

SPECT-CT is a key cardiac imaging technique that evaluates blood flow to heart muscle, identifying reduced perfusion and prior damage....

Blockchain Adoption Accelerates as SwissChain and Amundi Launch Tokenized Financial Solutions

SwissChain Holding SA has digitized its share certificates using blockchain, improving transparency, efficiency, and ownership tracking while maintaining Swiss legal...

|

|

|  |

|

|

-

Impact Investing2 weeks ago

Impact Investing2 weeks agoNet-Zero Asset Owner Alliance Introduces Transition Targets in Updated Climate Protocol

-

Business1 day ago

Business1 day agoGlobal Markets on Edge as Iran Conflict, Inflation Pressures, and Financial Risks Intensify

-

Impact Investing1 week ago

Impact Investing1 week agoESG Funds Still Hold BP Despite Shift Back to Fossil Fuels

-

Impact Investing6 days ago

Impact Investing6 days agoITAS Mutua Reports Strong 2025 Growth and Sustainability Progress