Featured

Is a government shutdown imminent? How the Trump Rally has made the market nervous

President Donald Trump has threatened to shut down the government, affecting the stock market in a negative way.

“If we have to close down our government, we’re building that wall. We’re going to have our wall. The American people voted for immigration control. We’re going to get that wall.” — Donald Trump, Phoenix rally, August 22, 2017

Last time we checked it was supposed to be Mexico that was paying for the wall. Now, it appears it is the American taxpayer. After all, someone has to pay for it.

We go away for a long weekend camping in the backcountry—no phones, no internet—and we return hoping that things got better. However, no such luck. We left with memories of Charlottesville, Virginia and returned with Phoenix, Arizona. Following months of what many have called the “Trump Rally,” the markets have decided to pause once again. The market paid attention to the words “close down our government.” Markets do not like negative statements.

The Phoenix statement was, however, positive for gold but negative for the US$ and interest rates (US Treasuries). Investors started dumping US Treasuries maturing into October 2017 just because they were nervous that they might not be paid. It is not as if anyone really expects the US government to shut down, but it should be noted the US has been through this before and there have been short-term shutdowns in the past. With Trump, no one knows what to expect.

Markets have paused before during the “Trump rally.” Since the February 2016 low we have seen the pause that ended with the “Brexit” mini-panic (April–June 2016), the election pause and mini-panic (August–November 2016), and the first strong signs that the Trump “agenda” might be in jeopardy (March/April 2017). After each pause, the market moved to new all-time highs. Given that the debate over the debt ceiling along with a budget that if not passed could result in the US government shutting down our sense says that this particular pause/correction won’t be over until at least October and possibly longer. Both the debt ceiling and the budget are supposed to be in place by October 1.

So what would shutting down the US government actually mean? According to some pundits, it would affect the following:

- Vacation spots: national parks, zoos, museums, etc. But not necessarily all, as many have entrance fees and could sustain themselves.

- Furloughing of employees: but not critical services such as air traffic controllers. It would affect, however, thousands of government employees and that in turn could have a negative impact on the economy.

- It won’t impact the military except civilians working for the military and possibly the National Guard.

- Taxes would still be collected.

- The mail would still be delivered, as the Post Office is self-funding.

- However, don’t count on getting your gun permit or your passport.

- Cheques expected from the government might not come except for social security, as it would be delivered.

- Finally, US Treasury issues would continue but it would not be able to raise any new money. Banks would remain open.

It is not as if this hasn’t happened before, either. Indeed it has been a somewhat regular occurrence since the Presidency of Ronald Reagan. Partial, short-term shutdowns occurred under Ronald Reagan (3), George H. W. Bush (1), Bill Clinton (2) including the longest ones, and Barack Obama (1). The shutdowns varied from 1 to 21 days. How did markets react then? Well during the last three shutdowns, the market was unfazed and actually rose. Overall, the market has only suffered a small loss because of the gamesmanship surrounding shutdowns. In the early days under Reagan, markets reacted negatively. Since the 1990’s, however, the markets have shrugged it off.

Because of the US separation of powers, the US Congress has the sole power of the purse and the appropriation of government funds. Once it is approved by Congress it goes to the Senate and then finally to the President. If the President refuses to sign it, it automatically becomes law. If he vetoes the bill then it goes back to Congress where a two-thirds majority could override the veto.

All previous shutdowns occurred when the Congress was a different party than the President. Our current President is a Republican as are Congress and the Senate. However, as has been seen—in particular on the failure to pass the health care repeal and replace–having all three levels in harmony has become rather meaningless. The Republican President, Donald Trump, has been continually at odds with the Republican controlled Congress and Senate, berating them both collectively and personally. None of it has succeeded in getting bills passed as sufficient Republicans joined Democrats in the Senate to ensure the defeat of bills.

Still, just the thought of a prolonged fight over the debt ceiling and the budget has made the market nervous. The market ignores Treasury Secretary Steven Mnuchin when he issues soothing words but the market is nervous when Trump threatens a government shutdown because of his unpredictability. A reminder that to date the Trump administration has achieved little of what they wanted unless Trump could do it by Presidential decree.

However, important things like funding, taxes, going to war, etc. are the prerogative of Congress, not the President. Co-operation and bi-partisanship are supposed to be the order of the day. Unfortunately, in the polarized world of the US today none of that appears to be present. Couple that with the unpredictability of Trump and markets may have a heart attack, okay a mild one. The result could see this end in a mini-panic.

The polarization is nowhere more present than on the streets where as demonstrated by Charlottesville, Virginia some believe the second civil war is underway. Irrespective of this, the crisis could well deepen as demonstrations and clashes continue. And the stock, bond, currency and metal markets will remain on edge. Fasten your seatbelts. We could be in for a bumpy ride.

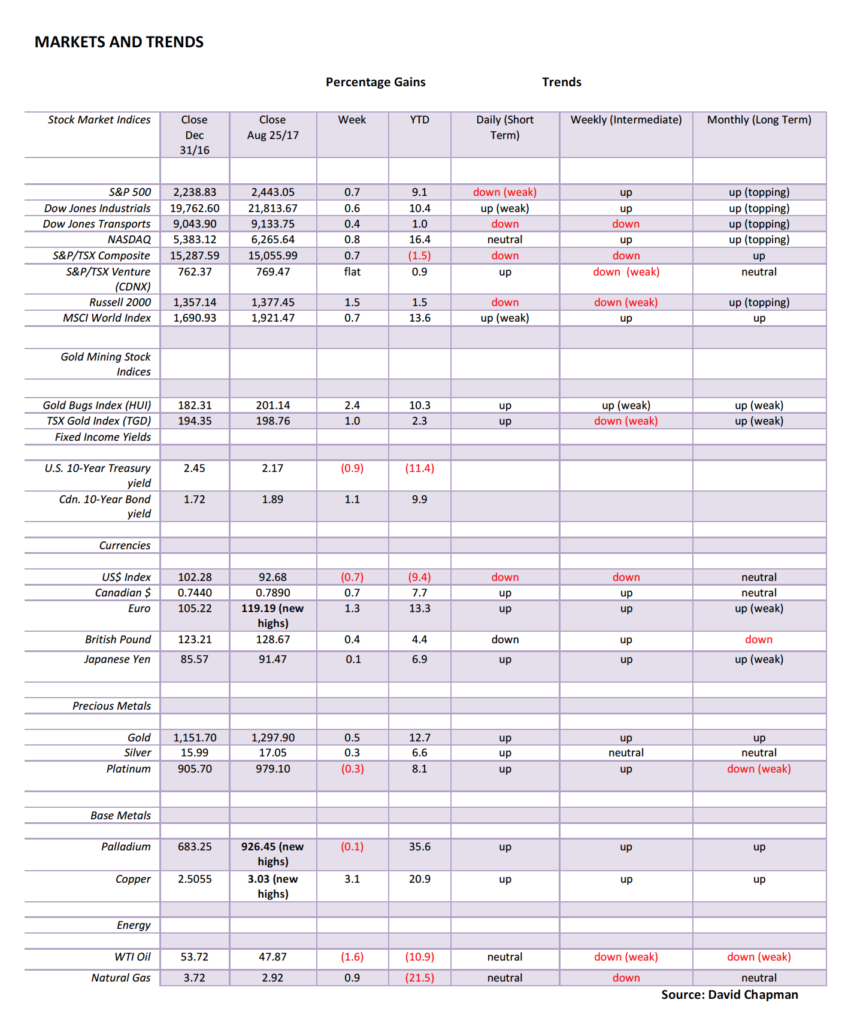

Markets and Trends © David Chapman

Note: For an explanation of the trends, see the glossary at the end of this article. New highs refer to new 52-week highs.

© David Chapman

We continue to believe that we have completed five waves up from the Brexit panic low. If that is correct then we should have completed wave 3 to the upside. Triggers were primarily the Charlottesville riots coupled with Trump’s Phoenix rally where he threatened to shut down the government if he didn’t get his way on the Mexican wall. But markets do not go straight down (or up). Janet Yellen’s speech at Jackson Hole, Wyoming has helped steady the markets. Rather than take a hawkish tone she was more measured. Trump economic advisor Gary Cohn also helped with some positive spin on the markets especially indicating that he expected tax reforms to pass and also that he did not intend on resigning. Following an initial negative reaction to Trump’s Phoenix speech, Yellen and Cohn helped calm the market.

All of this came against the background of Hurricane Harvey bearing down on the Texas coast and shutdowns in the US oil and gas industry including refineries that helped spike gas prices. Janet Yellen also issued a warning about messing around with the broad financial reforms that were put in place following the 2008 financial crisis. Reforms have helped stabilize the financial system and have made the banking system safer and more resilient. This would, of course, put her at complete odds with the Trump administration that wants to roll back many of these reforms. Yellen’s term is up in February 2018 and many fully expect she will not be back. Depending on who replaces her and how it is handled could calm markets or create a firestorm.

This past week was an up week for the US markets although it did little to break the recent trend that is shifting to the downside. The Dow Jones Industrials (DJI) gained 0.6%, the S&P 500 was up 0.7%, the NASDAQ gained 0.8% while the Dow Jones Transportations (DJT) jumped a more modest 0.4%. Elsewhere, however, things weren’t quite as rosy. The Chinese Shanghai Exchange (SSEC) jumped 1.9% and the London FTSE was up 1.1%, but the Paris CAC 40 dropped 0.2%, the German DAX was flat and the Tokyo Nikkei Dow (TKN) was off 0.1%. Toronto’s TSX Composite gained 0.7% while the TSX Venture Exchange (CDNX) was flat.

So what next? Our expectations are that the rebound in the latter part of the week was merely a bounce back following the recent down draft. At the recent low, the DJI was off 2% from its high of August 8, 2017. Small so far. The bounce back could even see new all-time highs once again but it is here where we might expect to see some divergences. The DJI might make new highs but no other index. That would be a non-confirmation. Key levels on the down side are seen at 21,700 for the DJI and 2,420 for the S&P 500. A firm break of 21,500 on the DJI and 2,400 for the S&P 500 would absolutely confirm that the top is in. Only new highs with each of the indices also making new highs would confirm that the uptrend is firmly in place.

Given the background of the ongoing turmoil in White House, odds would seem to favor the downside at this time. Seasonally we are also moving into the weakest time of the year. September is on record as being the weakest month of the year and October is notorious for crashes and panics. If we are correct that this is wave 4 up from the February 2016 low then odds favor once a low is found we should embark on wave 5, a wave that could take us into the first quarter of 2018.

© David Chapman

Here’s a closer look at the last six months of the DJI and the most recent five wave advance from the wave ((iv)) low seen in April 2017. Friday’s action that started out positively soon faded and by the end of the day the market had closed about where it started. The Japanese candlestick pattern left on the charts is known as a shooting star. It usually has bearish implications. If correct the markets should fall on Monday or at least fall this coming week. As noted a break and close under 21,700 should start to confirm the recent high on August 8, 2017.

© David Chapman

Here is the S&P 500/Russell 2000 ratio. The S&P 500 is considered to be a large cap index whereas the Russell 2000 is a small cap index. When the ratio is rising large caps are outperforming small caps. When the ratio is falling small caps are outperforming large caps. In a bear market, large caps tend to outperform whereas in a bull market small caps tend to outperform. Since December 2016 the S&P 500 has been outperforming the Russell 2000 despite both markets moving higher and even making new all-time highs.

Weakness in the small cap stocks is a potential harbinger of weakness to come in the large cap stocks. Since the market has been moving steadily higher since November/December 2016 one would expect the small caps to be leading. From roughly February 2016 onwards small caps were the leaders as was to be expected. But that has stopped in 2017 and now the large caps are leading. This we believe is another warning that the bull market of 2009 to 2017 could soon be coming to an end.

© David Chapman

After hitting a low of 9.35 (record low) in July the VIX volatility index spiked to around 16 in the recent decline. This was a level that had been seen before during corrections in April and May. But now the VIX is head down once again as the fear seems to have come out of the market. This is not to say it is going to make new lows. The VIX needs to fall under 10.5 to suggest that fear has been taken out of the market once again. Given the resistance at around 16, the VIX needs to break above that level to suggest that something more is going on than just a mild correction.

© David Chapman

The TSX Composite has been drifting downwards since making a top back in February 2017 long before the US indices were making tops. This drifting downward pattern has the look of a possible descending triangle. That suggests the TSX Composite should break to the downside. A break under 14,900 could start the breakdown but under 14,800 the breakdown could become more serious. Only a firm break above 15,400 might begin to shift the negative outlook. Real Estate and financials appear to be weakest looking sectors. Given financials importance in the TSX Composite, it might be worth battening the hatches a bit.

© David Chapman

The US Treasury market was rather mixed this past week following Trump’s Phoenix speech wherein he threatened to shut down the government if he didn’t get his way with the Mexican wall. The crucial dates are around October 1, 2017. In the event of a government shutdown, October 2017 US Treasury maturities were sold off. Why take a chance on that you might be paid. But then you might not. Longer dated maturities are not, however, subject to short-term market gyrations and as a result, the rebound that has been going on since March continued.

The longer dated maturities are seen as a safe haven. The ten year Treasury note ticked down 2 bp to 2.17% from 2.19% while the iShares 20 year Treasury bond ETF (TLT) rose roughly 0.6%. This appears to suggest that the rebound has more to go to the upside. It is possible the TLT could reach to 130 before it would run into a stronger wall of resistance. It could be that this C wave up is going to unfold in 5 waves.

So far we have seen only two and we could be working on wave 3. Or the C wave may have completed at 128.05 in June 2017 and this is merely a wave back following the first downdraft that bottomed at 122.32 in late June. A break below 125 could suggest that instead, bond prices would fall (yields rise as yields move inversely to prices). It is interesting to note that the Canadian ten-year government of Canada bond rose in yield this past week to 1.89% from 1.87%. Usually the two move in sync. When they don’t it might mean something else is in play.

© David Chapman

Spread watch. The two year – ten-year US Treasury note spread narrowed this past week to 0.82%. This is a reflection of tightening rates in the shorter terms and safe haven buying in the longer dates. The breakdown occurs under the June low of 0.78%. At 0.82% the spread is nowhere near levels that were seen prior to both the 2000-2002 and 2007-2009 recessions. Back then, spreads were negative. Inverse yield curves are more a sign of impending trouble. But following a rebound into July, the recent downward trend appears to be underway once again.

Note how the spread peaked roughly with the election in November 2016. Few pay attention to the bond market as a precursor to the economy. Widening spreads are showing confidence in the economy but falling spreads are showing some caution towards the economy even as on the surface all appears well. If the government does shut down on October 2017 because of failure to pass the debt ceiling and the budget then this spread should narrow even further. Further, a crisis over the debt ceiling and budget and a government shutdown also negatively affects the Federal Reserve and its ability to manage monetary policy.

© David Chapman

The US$ Index turned down once again this past week losing 0.7%. The prime beneficiary continues to be the Euro that jumped to new 52-week highs gaining 1.3%. The Canadian Dollar was also a beneficiary up 0.7% and back over 80 cents. Say what you will but Trump is having a negative impact on the US$ and that eventually should translate into trouble for the US stock and bond markets. If the recent rebound was our wave ((iv)) it was a pretty feeble one.

It did unfold in classic ABC fashion. But the breakdown under 93 suggests to us that we could well be starting the next plunge to new lows. The next target could well be 91.88, which was a low seen back in May 2016. Ultimate targets for wave ((v)) could be 91.10 but if we were to plunge under 91 then the target could be as low as 88. Only a rebound now that returns back above 94 could change this unfolding negative scenario.

The weakening US$ also means the Euro could continue to be a beneficiary of turmoil in the US. The Canadian Dollar should also continue to benefit. However, it is unlikely the British Pound would fare well due to concerns about the Brexit that is not going particularly well. Indeed the British Pound is in danger of falling below 1:1 with the Euro. The Japanese Yen would also benefit, as would the Swiss Franc.

© David Chapman

Given the turmoil surround Charlottesville and Trump’s Phoenix speech that suggested that he would shut down the government if he didn’t get his way with the Mexican wall it is probably not surprising that gold as one of the safe havens has jumped higher. Gold gained 0.5% this past week and is now up 12.7% in 2017 and is up 7.7% since the July 10, 2017 low of $1,204. Triple tops are a rare event so our senses tell us that gold should eventually carry through $1,300 and test the highs of July 2016 near $1,377. However, $1300 is at least initially proving to be tough resistance.

Since hitting a high of $1,307 on August 18, 2017 gold has been bouncing back and forth including a rather bizarre plunge to $1,278 on August 25, 2017. The plunge was caused by someone dumping 21,256 gold contracts in front of Janet Yellen’s speech at Jackson Hole, Wyoming. That is the equivalent of more than 2 million ounces of gold. But after Yellen spoke the US$ plunged and gold prices rose because her speech failed to contain any hawkish tones on US interest rates.

Indeed she appeared far more cautious. She parses her words carefully but there was clear concern about statements emanating from the President that could cause the Fed to act on the side of caution. The result was that December futures closed up almost $6 after being down almost $13. The reversal day bodes positively for gold going forward and we suspect that gold should break above $1,300 this coming week. Only a close below $1,265 might change our mind about gold prices moving higher. As of August 25, 2017, gold sentiment stood at around 55% putting it roughly in the middle.

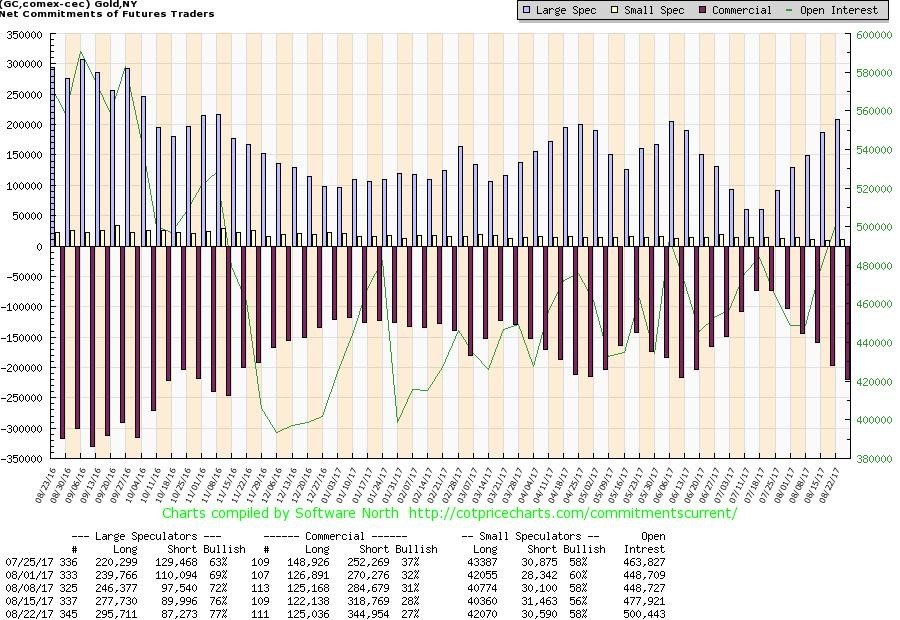

© David Chapman

The commercials seem to think gold is going to fall as the commercial COT fell this past week to 27% from 28% the previous week. Five weeks ago the commercial COT was at 37%. No doubt the recent fight at $1,300 is being led by the commercials who are once again trying to suppress the price. It doesn’t suggest that they will succeed but it keeps us guessing. If gold were to bust through $1,300 and stay above that point it might spark some short covering that would help fuel a further rally for gold. On the other hand, they could come right back in and try and slam gold down again.

The banksters or the crimesters as some refer them as are often a good sign of tops and bottoms in the gold market. We are reminded that during the bull run from 2009 to 2011 the commercial COT was almost continually under 30% and at levels that might have suggested a top. So they can be pushed back under the right circumstances. Short open interest jumped roughly 26,000 contracts this past week but long open interest was also up about 3,000 contracts. The large speculators (hedge funds, managed futures etc.) saw their COT rise to 77% from 76%. Usually I become concerned if they get over 80%. They are not there yet. The large speculators COT saw long open interest rise about 18,000 contracts and short open interest fall just over 2,000 contracts.

© David Chapman

If there is a concern about gold it is the failure of silver to clearly lead the way. Silver usually leads the market for the precious metals both up and down. This past week silver gained 0.3% vs. gold’s gain of 0.5%. On the year silver is only up 6.6% vs. gold up 12.7%. Silver has thus far failed to break out over its 200-day MA and over the downtrend line from the July 2016 high of $21.23. While silver’s short term trend has turned up the intermediate and long term trends remain locked in neutral.

Frustrating for all those who believe silver prices should be a lot higher. Silver at least now appears to be finding support in the $16.80/$17 zone. But the reality is silver needs to bust out over $17.50 to suggest higher prices. Over that level, there remains considerable resistance up to around $19. Silver has potential to rise to the $26/$27 zone if it succeeds. But it needs to regain above the July 2016 high of $21.23 to even think of that. Silver did diverge quite considerably at the July 10, 2017 low when silver prices plunged to new lows below its December 2016 low but gold failed to do so. It was a positive sign that suggested that a bottom might be in play. We would only become concerned if silver were to break down under $16.50.

© David Chapman

It is interesting to note that despite the weakness in silver prices vs. gold the commercial COT for silver is not as negative as the commercial COT for gold. The commercial COT for silver slipped to 33% this past week from 35% the previous week and 41% five weeks ago. Long open interest held steady but short open interest rose roughly 6,000 contracts. For the large speculators COT, it rose to 66% vs. 63% the previous week. Long open interest remained steady (as it has for weeks) and short open interest fell roughly 6,000 contracts. The high level of long open interest for the large speculators we view as positive as it suggests that many are holding silver for a long-term play. Usually, they liquidate when silver prices are weak.

© David Chapman

While the gold stocks continue to be frustrating our outlook remains positive. The past few weeks we believe we are witnessing a stealth rally in gold stocks. We are up about 8% from the July 2017 low but no one is paying any attention. Grant you they haven’t given us a lot of reason to pay attention. The TSX Gold Index (TGD) is up a feeble 2.3% in 2017. Pitiful really. Even the US index known as the Gold Bugs Index (HUI) is up 10.3% in 2017. Possibly part of the reason is that Tahoe Resources (THO-TSX) a giant silver mining company plagued with legal problems at its Guatemala mine, a mine that is one of the largest silver mines in the world. Tahoe is down 69% in the past year.

But Tahoe is not alone showing considerable weakness in the TGD over the past year. Others include TMAC Resources (TMR) down 51%, Yamana Gold (YRI) off 40%, Klondex Gold (KDX) down 42%, Semafo (SMF) down 43%, Sibanye (SAGL) off 47%, Harmony Gold (HMY) down 54%, Guyana Goldfields (GUY) down 51%, Detour Gold (DGC) off 47% and Eldorado Gold (ELD) down 47%. It is noteworthy that only Sibanye, Eldorado, and Harmony are components of the HUI. If gold prices rise as we suspect then eventually these companies will play catch up. And that catch up could be spectacular as they have considerable room to rise.

The TGD needs to break out firmly over 200 and preferably over 210 to suggest higher prices. The TGD has potential to rise to 400 but it first has to regain the August 2016 highs of 283.

© David Chapman

Sentiment towards the gold stocks remains closer to depression than it does to happiness. Above is the Gold Miners Bullish Percent Index (BPGDM). Depression is readings below 25 and happiness is readings above 75. At 28.57 it is closer to depression. Gold stocks are unwanted and unloved. And that normally suggests to us that gold stocks should be owned. We’ll sell when everyone is happy. But we are long ways away from happiness.

GLOSSARY

Trends

- Daily – Short-term trend (For swing traders)

- Weekly – Intermediate-term trend (For long-term trend followers)

- Monthly – Long-term secular trend (For long-term trend followers)

- Up – The trend is up.

- Down – The trend is down

- Neutral – Indicators are mostly neutral. A trend change might be in the offing.

- Weak – The trend is still up or down but it is weakening. It is also a sign that the trend might change.

- Topping – Indicators are suggesting that while the trend remains up there are considerable signs that suggest that the market is topping.

- Bottoming – Indicators are suggesting that while the trend is down there are considerable signs that suggest that the market is bottoming.

(Featured image by Gage Skidmore via Wikimedia Commons. CC BY-SA 2.0. All charts are courtesy of Stock Charts and COT Price Charts.)

__

DISCLAIMER: David Chapman is not a registered advisory service and is not an exempt market dealer (EMD). We do not and cannot give individualized market advice. The information in this article is intended only for informational and educational purposes. It should not be considered a solicitation of an offer or sale of any security. The reader assumes all risk when trading in securities and David Chapman advises consulting a licensed professional financial advisor before proceeding with any trade or idea presented in this article. We share our ideas and opinions for informational and educational purposes only and expect the reader to perform due diligence before considering a position in any security. That includes consulting with your own licensed professional financial advisor.

Temenos to Acquire Additiv to Boost AI Wealth Management

Temenos is acquiring Zurich fintech Additiv to strengthen its digital wealth management and expand AI-driven financial orchestration. Additiv’s platform connects...

EFPIA Warns Limited SPC Reform Could Weaken EU Pharma Competitiveness

EFPIA supports the EU Biotechnology Law and a 12-month SPC extension but warns the current proposal is too limited. A...

EU Approves €23B Italian Renewable Energy Plan to Boost Climate Goals

The European Commission approved Italy’s €23 billion aid scheme to boost renewable energy and meet 2030 climate goals. Supporting wind,...

Institutional Bitcoin Buying and LiquidChain Presale Signal Market Optimism

Institutional Bitcoin buying, like Strategy’s 1,550 BTC purchase, signals confidence, stabilizes prices, and may trigger bullish momentum. Meanwhile, infrastructure projects...

The German Biotech Industry Faces Funding Crunch Despite Market Stability

German biotech held steady in 2025 but faces ongoing financing pressures, according to EY-Parthenon and BIO Deutschland. Total capital fell...

|

|

|  |

|

|

-

Fintech1 week ago

Fintech1 week agoRevolut Begins Controlled India Rollout Targeting Massive UPI Payments Market

-

Crypto2 weeks ago

Crypto2 weeks agoCrypto Market Mixed as Bitcoin and Ethereum Slip Amid Rising Volatility

-

Biotech3 days ago

Biotech3 days agoTG Therapeutics Advances Subcutaneous Briumvi With Strong Trial Results and Rising Sales Momentum

-

Crypto1 week ago

Crypto1 week agoAltcoins Show Mixed Performance as Bitcoin Weakens

You must be logged in to post a comment Login